In a world of flexible payments and instant approvals, more shoppers are asking the question: buy now, pay later vs credit card, what’s the better option?

Both offer ways to spread out your purchases over time, but they differ in how they work, how they impact your credit, and what you’ll ultimately pay.

Whether you’re trying to manage your cash flow, build woyour credit history, or avoid interest charges, understanding the pros and cons of each can help you make the right choice. I did the research; here’s what you need to know from someone who’s used both.

Key Takeaways

- BNPL Offers Predictable Payments: Buy Now, Pay Later plans typically include fixed, interest-free installments—ideal for short-term purchases.

- Credit Cards Build Credit Faster: Credit cards report to all major credit bureaus, helping you build credit with consistent, responsible use.

- Fees and Interest Vary: BNPL may charge late fees, while credit cards can rack up interest and penalties if balances aren’t paid in full.

- Rewards vs. Simplicity: Credit cards often offer rewards and perks; BNPL is simpler and more budget-friendly but lacks long-term benefits.

- Choose Based on Spending Habits: Your choice should depend on your credit goals, payment discipline, and purchase size.

How Buy Now, Pay Later Works

Buy Now, Pay Later (BNPL) lets you divide a purchase amount into smaller, scheduled payments—typically four interest-free installment payments over six weeks. Some BNPL services also offer longer payment plans with monthly payments and may charge interest depending on the provider and terms.

Popular BNPL providers include Afterpay, Klarna, Sezzle, and Affirm, though Sezzle is my provider of choice. Approval is usually quick, and many use only a soft credit check (if any), which doesn’t affect your credit score.

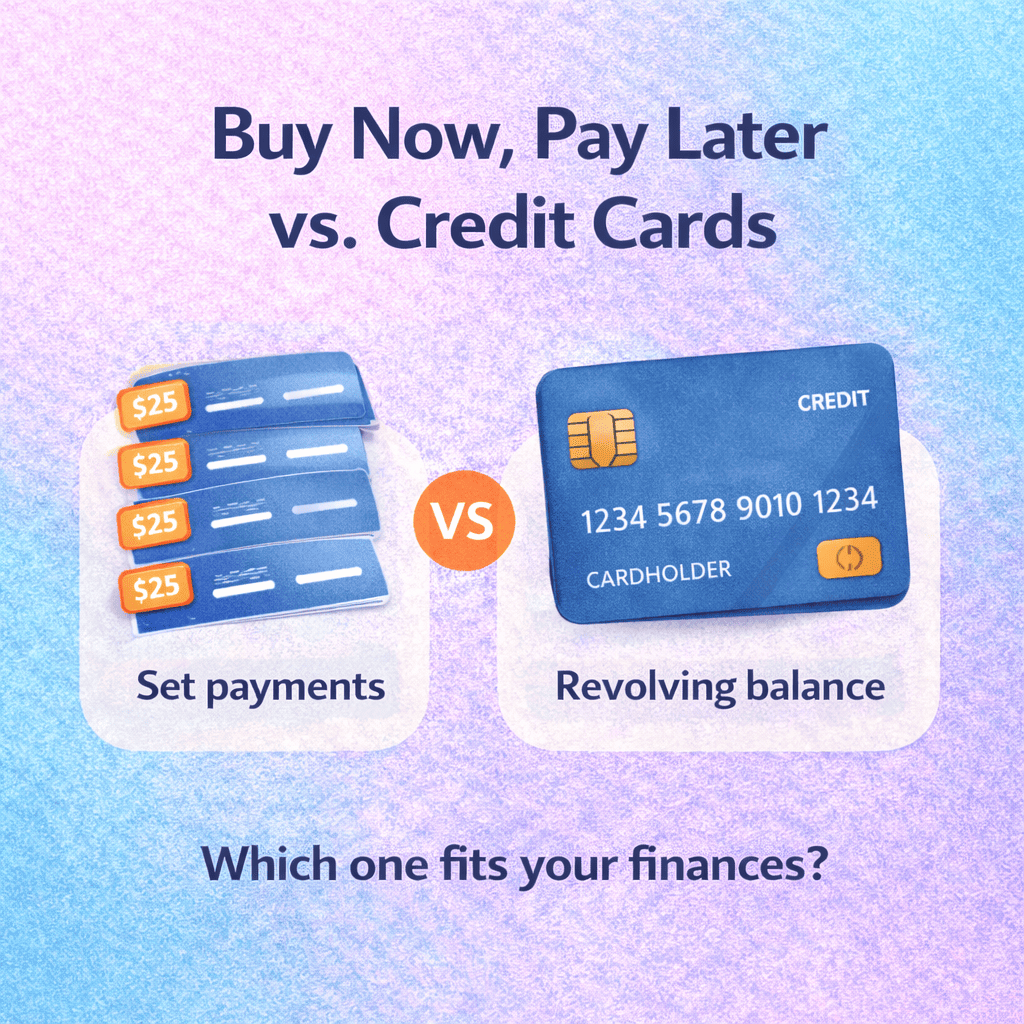

With BNPL plans, there’s no revolving credit or ongoing balance—you’re committing to a fixed schedule at the point of sale, with clear repayment dates.

How Credit Cards Work

Traditional credit cards give you access to a revolving line of credit with a credit limit. When you make a purchase, you can choose to pay the full credit card balance by the end of the billing cycle or carry a remaining balance into the next month by making minimum payments.

This flexibility comes at a cost: if you don’t pay in full, you’ll likely incur interest charges, which can add up fast. Late fees, foreign transaction fees, and high APRs are also common.

However, major credit cards also offer valuable perks like credit card rewards, fraud protection, and credit-building benefits—especially when reported to the three major credit bureaus: Experian, Equifax, and TransUnion.

Key Differences: Buy Now, Pay Later vs Credit Card

| Feature | Buy Now, Pay Later | Credit Cards |

|---|---|---|

| Interest | Usually none (short-term plans) | Often charged on carried balance |

| Payments | Fixed, scheduled payments | Flexible; minimum or full payments allowed |

| Approval | Often no or soft credit check | Usually requires a full credit check |

| Credit Building | Limited, depends on provider | Reported to major credit bureaus |

| Fees | Possible late payment fees | Late fees, interest, and other charges |

| Rewards | No | Yes (with many major credit card issuers) |

| Usage Flexibility | One-time per transaction | Ongoing access until credit limit is reached |

Pros and Cons: BNPL vs. Credit Cards

Pros and Cons of BNPL

Pros

- Interest-free short-term plans

- No hard credit check for most services

- Clear fixed payments make budgeting easier

- Great for people with a low credit score or limited history

- No risk of long-term credit card debt

Cons

- Late payment fees can apply if you miss a payment

- May not report to credit bureaus, so won’t build credit

- Easy to overspend with multiple BNPL plans

- Less protection compared to major credit cards

- Fewer perks—no earn rewards or cash back

Pros and Cons of Credit Cards

Pros

- Builds credit history if used responsibly

- Offers credit card rewards like points, miles, or cash back

- Widely accepted and more secure for online purchases

- Grace period before interest charges apply

- Helps with emergency purchases if you’re short on cash

Cons

- High interest rates if you carry a balance

- Potential for long-term debt from minimum payments

- Missed or late fees can hurt your credit score

- Can tempt overspending and raise credit utilization

What About BNPL Loans and Installment Loans?

Some BNPL services offer longer payment plans that resemble installment loans—often with a fixed interest rate and terms from 6 to 48 months. These work more like traditional financing and may report to credit bureaus, especially if you miss a payment.

That means a BNPL loan can potentially build credit—or damage it—depending on how it’s handled.

By contrast, installment loans like personal loans typically have longer repayment periods and higher approval requirements, but they often offer more consumer protection and lower interest rates compared to high-APR credit cards.

Choosing the Right Option

Here’s how to decide between BNPL and credit cards, based on your goals:

- For budget control: BNPL is better, thanks to fixed payments and upfront repayment terms.

- To build credit: Credit cards are better, since most report to major credit bureaus.

- If you want rewards: Credit cards win with cash back, points, or travel perks.

- For short-term financing: BNPL works great for smaller purchases that you can repay quickly.

- To cover emergencies: A credit card offers reusable credit and is better for unexpected costs.

Watch Out for the Downsides

With both options, missed payments can lead to trouble. BNPL payments may seem manageable, but juggling multiple plans can strain your budget. Likewise, paying only the minimum payments on a credit card can trap you in a long cycle of interest and debt.

It’s also important to know that credit card issuers and BNPL providers vary. Some BNPL services report to credit bureaus or offer later plans with higher fees. Meanwhile, not all major credit card issuers offer the same perks or protections.

Should You Use Both?

Many consumers use both. I do. Mainly, I use BNPL for specific purchases and major credit cards for everyday spending to earn rewards. If you manage them responsibly, you can enjoy the best of both worlds: the structure of BNPL plans and the flexibility of revolving credit.

Just avoid stacking payments across multiple services or maxing out your credit card balance, which can raise your credit utilization and lower your score.

Final Thoughts

When comparing buy now, pay later vs credit card, there’s no one-size-fits-all answer; it really depends on you, your spending habits, and what you’re looking to purchase. BNPL is ideal for smaller, predictable purchases, especially if you want interest-free financing without a credit check. Credit cards, on the other hand, offer flexibility, protection, and credit-building potential—but can cost you more if not managed wisely.

The best approach? Know your spending behavior, understand your payment responsibilities, and choose the option that supports your financial goals, not just what’s convenient at checkout.

If you’re looking to split your next purchase into easy, interest-free payments, download the Sezzle app today and pay smarter.

FAQs

BNPL splits purchases into fixed payments with little or no interest, while credit cards offer a revolving credit line that may accrue interest.

Only some BNPL providers report to credit bureaus. If they don’t, your payments won’t affect your credit score at all—positively or negatively.

BNPL short-term plans are usually interest-free. Credit cards often charge interest unless you pay your full balance each billing cycle.

It depends. BNPL is better for small, one-time purchases. Credit cards offer more flexibility and credit-building benefits, but require more discipline.

Yes, many people use both. Just be careful not to overextend your finances by juggling multiple payment plans or maxing out your credit limit.