Let’s set the scene. You’re checking out on a website, and the total is… not ideal. But there’s another option that you’ve been considering: pay in four. In just a few easy, interest-free installments, you can cut down how much you have to pay today; instead, you can spread out that payment over time, so you’re not temporarily as strapped for cash.

But how does buy now, pay later really work—and is it worthwhile for consumers?

As a BNPL user myself, I wrote this guide to walk you through how BNPL services operate, tell you everything you need to know about interest, fees, and repayment terms, and help you decide whether this is a good payment method for you.

Key Takeaways

- Flexible Payment Options: BNPL splits purchases into bi-weekly or monthly payments, often with zero interest.

- Fast and Easy Approval: Most BNPL providers use a soft credit check, so your credit score isn’t impacted upfront.

- Two Plan Types: Choose between short-term interest-free plans or longer-term monthly financing with fixed interest rates.

- Fees Can Apply: Missed or late payments may result in late fees or other service charges.

- Credit Impact Varies: BNPL may affect your credit if providers report to credit bureaus—positively or negatively.

What Is Buy Now, Pay Later?

Buy Now, Pay Later is a type of short-term financing that lets you split the cost of a purchase into smaller, more manageable chunks. Instead of paying the full purchase price upfront, you agree to a repayment plan—usually with bi-weekly payments or a monthly payment option.

BNPL plans are offered by third-party BNPL providers such as Affirm, Klarna, Afterpay, and PayPal Pay Later. Many of these providers are integrated directly into online checkout pages or retail apps.

Personally, while I tend to shy away from using it on day-to-day buys, BNPL has made a big difference for me in covering larger purchases, from gaming consoles to four-figure vet bills.

How Does Buy Now, Pay Later Work?

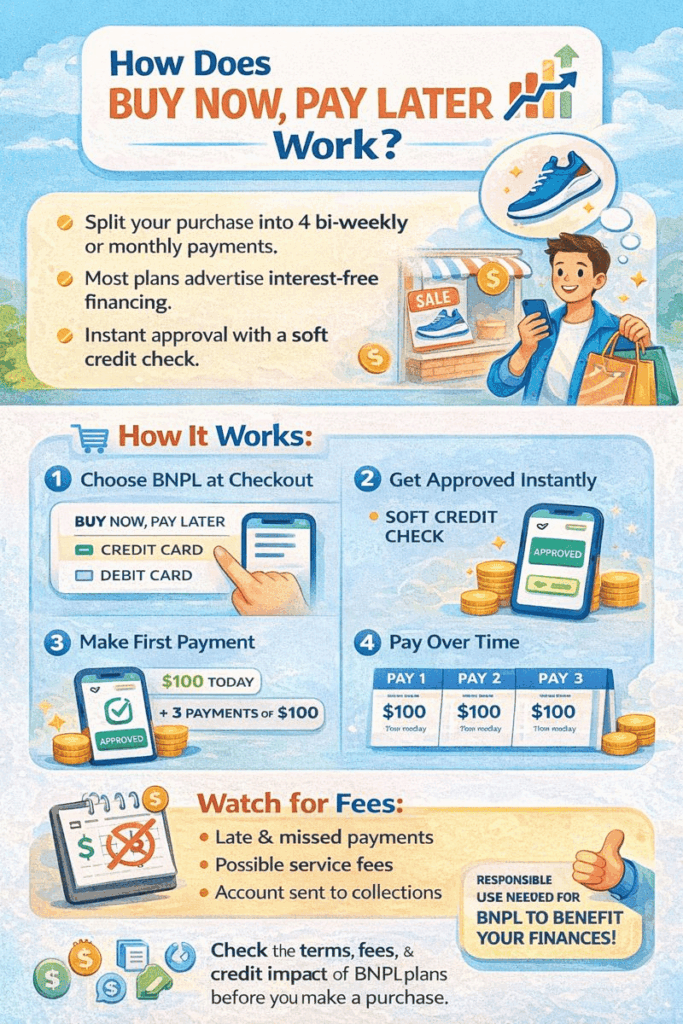

Here’s how the typical process goes:

- Choose BNPL at Checkout: Instead of using a credit card or debit card, you select a BNPL service as your payment method.

- Get Approved Instantly: Most providers do a soft credit check (which won’t affect your credit score) to determine eligibility.

- Make the First Payment: In most cases, you’ll pay 25% upfront.

- Pay Over Time: The remaining balance is split into equal interest-free payments, often over six weeks (e.g., four bi-weekly payments), or into longer monthly payment plans.

What Are the Main Types of BNPL Plans?

BNPL services usually fall into two main categories:

| Plan Type | Typical Structure | Interest? | Best For |

|---|---|---|---|

| Pay in 4 / Bi-weekly | 4 equal payments over 6 weeks | No (usually) | Small to mid-size purchases |

| Pay Monthly | Spread payments over 3–48 months | Yes (fixed interest rate) | Large purchases, more flexibility |

Short-term interest-free installments are great for budgeting without the commitment of a credit card, while longer-term BNPL loans with a fixed interest rate resemble personal loans or installment loans.

Are There Any Fees?

Yes, and this is where BNPL users should pay close attention.

While most BNPL plans advertise zero interest, many do come with additional fees such as:

- Late fees for missed payments or late or rescheduled payments

- Potential service fees for certain providers

- Some may charge for using a bank account or certain cards

These charges don’t always appear upfront, so always read the terms before clicking “Confirm.”

Does BNPL Affect Your Credit?

BNPL’s impact on your credit history and credit score depends largely on whether the provider reports your activity to credit bureaus or credit agencies.

Most BNPL services perform a soft credit check during the approval process, which does not affect your credit score. While this makes it easy to qualify, it also means that using BNPL won’t necessarily help build your credit unless the provider reports on-time payments.

However, not all providers do. If a BNPL service doesn’t share your payment history with the bureaus, consistent payments won’t boost your credit. On the other hand, missed payments can hurt your credit score—but only if the provider reports delinquencies or sends your account to collections.

Some BNPL apps, such as PayPal Pay Later, are beginning to expand their reporting policies. Still, not all BNPL providers report activity—at least, not yet—so the impact on your credit can vary widely.

BNPL vs. Loans or Credit Cards

BNPL is often compared to credit cards or personal loans, but there are key differences:

- Credit cards revolve, meaning you can borrow repeatedly; BNPL is tied to specific purchases.

- Personal loans offer larger amounts with structured repayment terms and consistent interest rates.

- BNPL is generally easier to qualify for, but offers less protection and fewer benefits.

Is BNPL Right for You?

BNPL can be a smart payment option when used responsibly. It’s best for:

- Budget-conscious shoppers avoiding large upfront costs

- Those with limited access to credit

- Users who are confident they’ll make on-time payments

It’s not ideal if you:

- Tend to overspend

- Miss due dates

- Are juggling multiple BNPL plans across different providers

Final Thoughts

So, let’s sum it up: how does Buy Now, Pay Later work?

Well, BNPL is a modern payment method that splits your purchases into manageable pieces—often with interest-free payments and minimal upfront requirements. But beneath the convenience lies the need for responsibility: missing payments or misunderstanding repayment terms can lead to late fees, damaged credit history, and other consequences.

Used wisely, though, BNPL can be a helpful tool for financial flexibility; in particular, making those big purchases more manageable, from groceries to little luxuries. Done well, buy now, pay later services like Sezzle can be a great addition to your financial strategy.

FAQs

It lets you split your purchase into smaller payments over time, often starting with 25% down and the rest paid in installments.

Not always. Most short-term plans are interest-free, but monthly financing options may include a fixed interest rate.

Yes, but only if the provider reports your payment activity to credit bureaus. Missed payments can hurt your score.

Most BNPL providers only run a soft credit check, which doesn’t impact your credit score.

You may be charged a late fee and lose access to future BNPL services. Repeated missed payments could affect your credit.