If you’ve already used buy now pay later, you probably understand the basics of splitting a purchase into four payments. But now Sezzle offers Pay in 5—and if you’ve seen it at checkout, you might be wondering what actually changes.

At its core, Pay in 5 is just an extended version of Sezzle’s installment model. Instead of four payments over six weeks, you spread the purchase over five scheduled payments with a slightly longer payment period. However, there are some new factors to consider with Pay in 5 before choosing it over Pay in 4.

So let’s break down exactly how Pay in 5 works, how it compares to Pay in 4, and which is the better option for you.

Key Takeaways

- Flexible Installments: Pay in 5 splits your purchase into five scheduled payments instead of four.

- Smaller Payments: Because the purchase amount is spread across more installments, each payment may feel more manageable.

- Soft Credit Check: Approval uses a soft credit check, not a hard credit pull.

- Possible Fees: Some extended financing options may include a disclosed service fee.

- Best for Larger Purchases: Pay in 5 can make sense when smoothing out cash flow on a bigger expense.

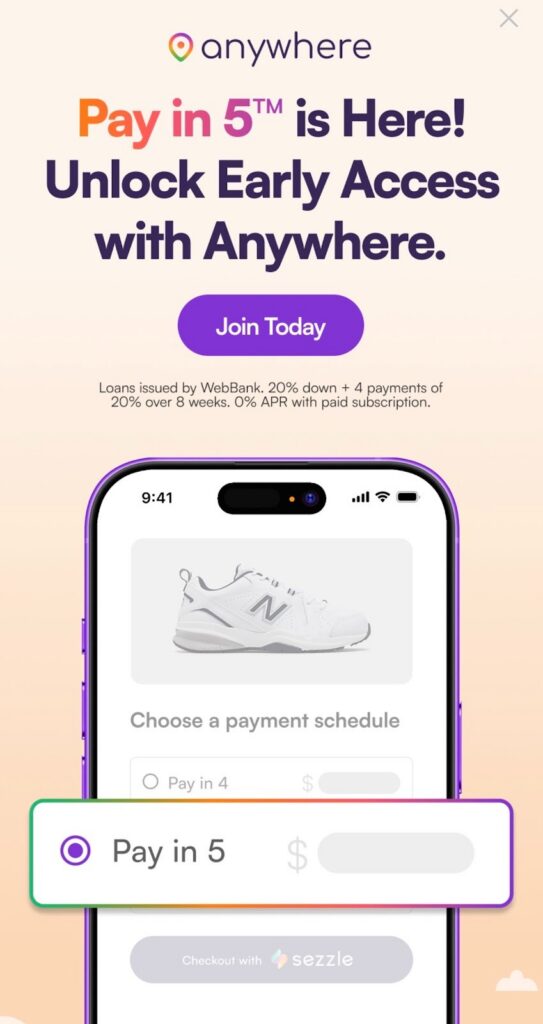

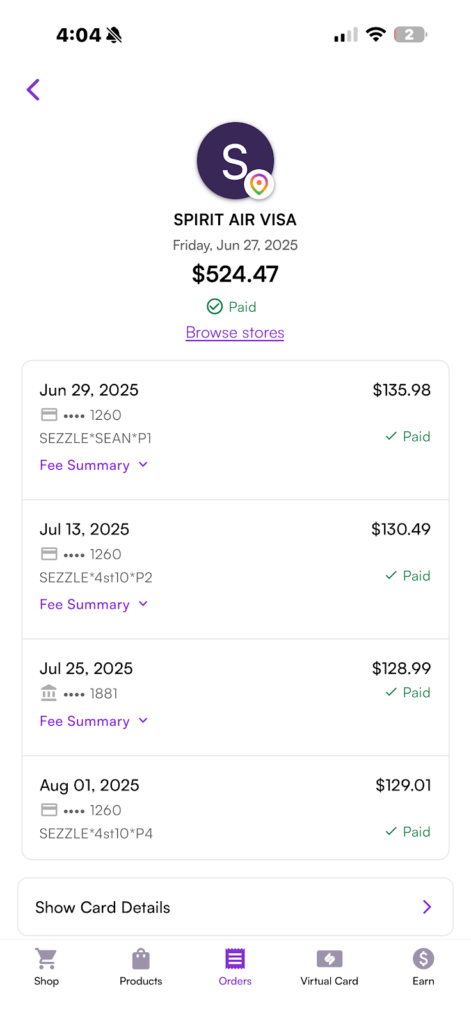

How Pay in 5 Works

When I selected Sezzle at checkout and chose the Pay in 5 option, here’s what happened:

- I made my first 20% payment immediately.

- Then, the remaining balance was divided into four additional payments.

- Payments are automatically drafted from my chosen payment method, like a debit card or linked bank account (I chose a card).

I could see the full purchase price, payment schedule, and any applicable fees before confirming. Like other Sezzle payment plans, approval typically involves a soft credit check; there’s no hard credit check just to see if you qualify.

Pay in 5 vs. Pay in 4: What’s the Difference?

The structure between Pay in 5 and Pay in 4 is nearly identical; the main difference is timing.

Pay in 4

- Four equal payments

- Usually completed within about six weeks

- Typically interest-free, but can have a service fee

Pay in 5

- Five scheduled payments

- Longer payment period

- Interest charges and fees depend on the contract

Practically speaking, Pay in 5 lowers the size of each installment by spreading the purchase across an additional payment. That can make a large purchase feel more manageable from month-to-month.

When Pay in 5 Makes Sense

Pay in 5 may be helpful when:

- You’re making a bigger purchase.

- You want smaller, more manageable chunks.

- You’re smoothing out short-term cash flow.

To be clear, Pay in 5 is still a structured installment plan with equal monthly payments; it isn’t an open-ended credit card balance. You’re committing to fixed payments over a set period. That said, stacking multiple BNPL payments at once can become harder to track. Like any financing option, discipline matters.

Fees and What to Watch For

Pay in 5 is generally available to users enrolled in Sezzle’s paid subscription plan (Sezzle Premium/Sezzle Anywhere). Not all shoppers will see this option at checkout, and eligibility depends on account status and subscription level. The best way to become eligible? Use Pay in 4 to build a reputable account history and view your purchase options for items over $50.

Sezzle’s standard Pay in 4 plan is interest-free. With Pay in 5 and certain extended products, a service fee may be disclosed before checkout, but there is no interest. If you miss payments, you could face late fees or temporary account restrictions.

Final Verdict: Is Pay in 5 Worth It?

Pay in 5 doesn’t reinvent how BNPL works; it just adds more flexibility to the buy now, pay later model. Spreading your purchase over five installments instead of four makes payments smaller and extends the timeline, letting each paycheck stretch a little further.

For consumers who want to avoid traditional credit card interest but need more breathing room than Pay in 4 allows, Pay in 5 with BNPL services like Sezzle can be a practical option.

FAQs

Standard Pay in 4 and Pay in 5 installment payment plans are usually interest-free.

Approval uses a soft credit check, which doesn’t negatively affect your credit score as long as you make your weekly or monthly payments.

It depends on your purchase size and cash flow. Pay in 5 offers smaller payments over a longer period.

Availability depends on eligibility and merchant participation within the Sezzle platform.

As with most BNPL providers, if you miss a payment, you may incur late fees and have your account temporarily restricted.