With all the news about Honey coming out right now, it’s more important than ever to be skeptical of financial services that seem too good to be true.

Sezzle is a buy now, pay later app that falls into that category, offering interest-free installments that allow you to pay for what you want over time, from groceries to designer bags. But if you’re anything like me, your eyebrows are—justifiably—raised.

cHow does Sezzle make money if it’s offering interest-free payments?

Let’s break down Sezzle’s business model, how it operates, and why this financial technology company has managed to grow into a publicly traded company with millions of users and merchant partners.

Key Takeaways

- Merchant-Funded Model: Sezzle primarily earns money by charging merchants a fee per transaction, not consumers.

- Interest-Free Perks: Most Sezzle payment plans offer zero-interest options, making it budget-friendly for responsible shoppers.

- Consumer Fee Revenue: While most users avoid interest, Sezzle collects revenue through late fees, rescheduling fees, and service charges.

- Credit-Friendly Approach: Sezzle uses soft credit checks and offers optional credit reporting through Sezzle Up.

- Tech-Driven Growth: As a financial technology company, Sezzle scales through smart risk assessment, platform integration, and investor backing.

What Does Sezzle Do?

Sezzle provides short-term financing options at checkout, allowing customers to spread their payments over time. Its most popular offerings are the Pay in 4 and Pay in 2 plans. With Pay in 4, users pay 25% upfront and the rest in three equal biweekly payments. Pay in 2 splits the cost into two payments spaced two weeks apart. These plans are interest-free, making them attractive to consumers looking to manage their budgets without using credit cards.

There’s also a Pay Monthly option for longer-term purchases (3–48 months), which comes with interest rates that can go as high as 34.99% APR. Obviously, the other options are more attractive, but it’s nice to know everything that’s available regardless.

So far, it sounds like a win for the customer—but what about Sezzle?

Sezzle’s Revenue Streams

Sezzle’s income primarily comes from merchant fees, consumer fees, and other value-added services. Here’s how it works:

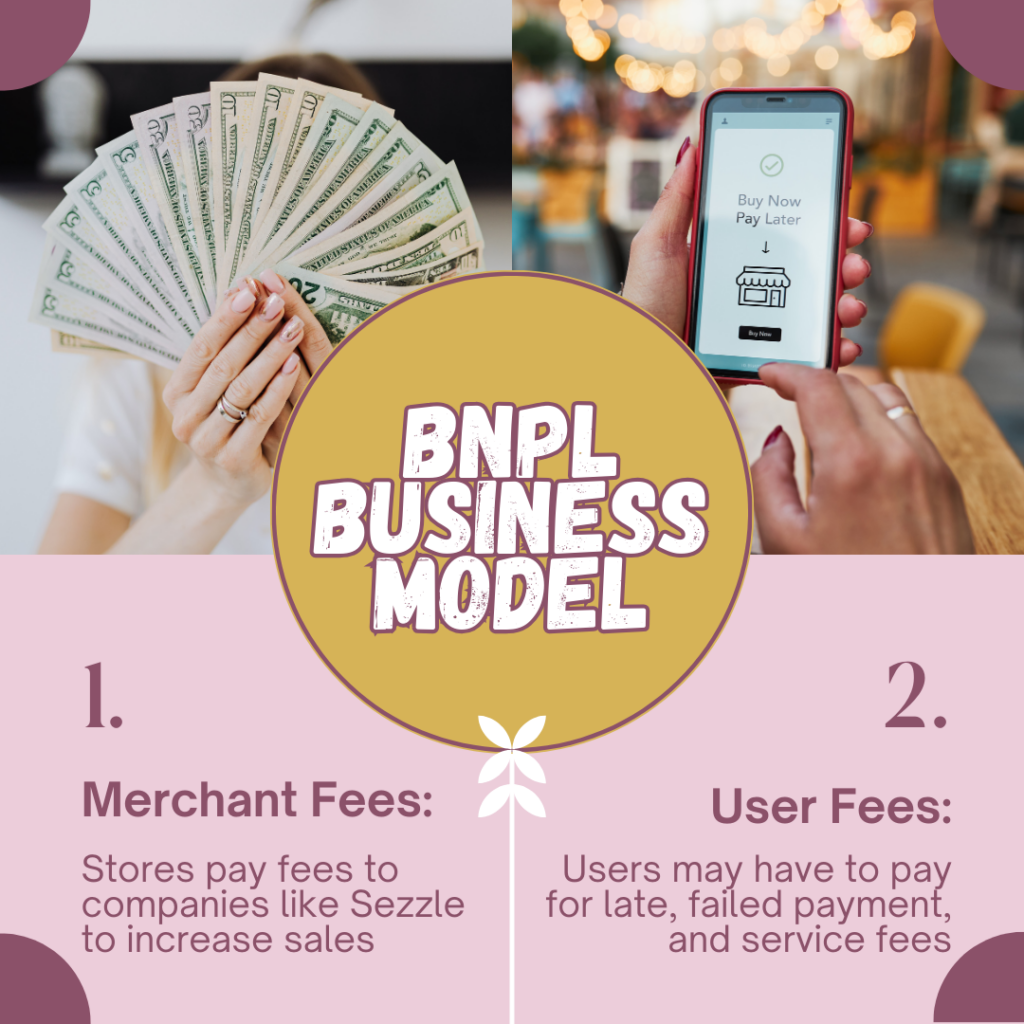

1. Merchant Fees: The Core Revenue Source

Sezzle’s main income comes from charging transaction fees to merchants every time a customer uses Sezzle to make a purchase. Retailers typically pay between 3–7% per transaction. This might seem high, but it’s a cost they’re willing to accept because Sezzle helps boost sales by giving shoppers more payment options and increasing average order values.

Because Sezzle assumes the risk of consumer non-payment, these merchant fees are the primary engine behind Sezzle’s revenue.

2. Consumer Fees: The Penalties and Extras

While Sezzle emphasizes interest-free installment plans, that doesn’t mean it’s completely fee-free for users. Here are some common fees that generate revenue:

- Late fees: Up to $15 per missed payment

- Failed payment fees: Up to $5

- Convenience fees: Up to $2.50 for using a debit card on payments beyond the first

- Rescheduling fee: One free change per order, then up to $7.50 each

- Service fee: Up to $5.99 for using the virtual Sezzle card

Though Sezzle doesn’t charge interest fees on most of its offerings, these smaller charges can add up, especially for users who miss due dates or change their payment schedule often.

That said, Sezzle is fairly transparent and doesn’t hit users with hidden fees—a key part of its appeal to budget-conscious consumers.

| Revenue Stream | Description | Who Pays | Typical Fee Amounts |

|---|---|---|---|

| Merchant Fees | Transaction fees are charged to retailers when customers use Sezzle | Merchants | ~3% to 7% per transaction |

| Late Fees | Charged when a user misses a scheduled payment | Consumers | Up to $15 |

| Failed Payment Fees | Applied when a payment attempt fails (e.g., insufficient funds) | Consumers | Up to $5 |

| Convenience Fees | Charged for using a debit card after the first installment | Consumers | Up to $2.50 |

| Rescheduling Fees | Fee for changing a payment date more than once per order | Consumers | One free per order; up to $7.50 after |

| Service Fees | Applied to one-time virtual card use | Consumers | Up to $5.99 |

| Interest on Long-Term Plans | Interest applied to “Pay Monthly” financing options | Consumers | Up to 34.99% APR |

How Sezzle Benefits Consumers

Sezzle appeals especially to younger consumers who might not have access to traditional credit or who someone who prefers not to use credit cards. Features like:

- Four interest-free payments

- Soft credit checks (with no impact on credit score)

- Access to credit-building tools via Sezzle Up

- No interest fees on short-term plans

…make Sezzle an great option for those trying to build financial freedom and practice responsible spending.

The Sezzle app is also well-designed, offering clear payment tracking, reminders, and the ability to reschedule if needed (once per order for free). Consumers can use Sezzle at partner retailers or anywhere Visa is accepted with the virtual Sezzle card, broadening its service offerings significantly.

Scaling Through Technology and Trust

As a financial technology company, Sezzle has built its platform to efficiently handle millions of transactions while minimizing payment defaults. While the company takes on the risk of non-payment, it uses algorithms and transaction history to approve customers and set spending limits. These limits start low and rise as users demonstrate on-time payments.

Sezzle reports to credit bureaus only if users opt into Sezzle Up, which can either help build credit history or damage it if payments are missed.

The company has also been able to integrate Sezzle into major e-commerce platforms, making it easy for merchants to accept payments through their existing checkout systems.

Why Merchants Work With Sezzle

Even with the 3–7% processing fee, merchants see the value. Sezzle helps increase conversions and reduce cart abandonment. In industries like fashion, beauty, and lifestyle—where impulse buying is common—giving consumers flexible payment options can make the difference between a sale and a bounce (and a bounce isn’t just a lost sale; it’s wasted ad spend).

In addition, Sezzle aims to support businesses focused on sustainability, community values, or ethical practices—traits that resonate with their younger audience.

Growing Through Funding and Partnerships

To scale its operations, Sezzle raised capital through private investors and eventually became a publicly traded company, giving it the financial backing to expand its services, hire talent, and innovate.

It has attracted institutional investors thanks to its growth, loyal user base, and clear differentiation in a competitive BNPL market.

How Sezzle Actually Operates as a Business

At its core, Sezzle lets shoppers split purchases into interest-free payments while earning revenue primarily from the businesses that offer it at checkout. Rather than relying on high consumer fees, Sezzle focuses on merchant partnerships, with additional income coming from optional services and select user features.

What sets Sezzle apart is how it manages risk while encouraging responsible spending. Through real-time approval technology, flexible payment options, and the ability for users to opt into credit reporting, the platform creates a system where customers feel supported—not pressured—and merchants benefit from higher conversions and repeat sales.

Final Thoughts

Sezzle’s business model shows how financial technology can evolve beyond traditional lending. By centering transparency, flexibility, and user control, Sezzle has positioned itself as more than a payment option—it’s part of a broader shift in how people manage everyday spending.

By offering interest-free payments with no hard credit check, they’ve lowered the barrier to entry for millions of consumers while still building a sustainable, profitable company. The best companies deliver a win-win: the customers win, so they keep using the business. That’s exactly what Sezzle has created for responsible spenders.

So, let’s recap: Sezzle’s profit structure is a mix of merchant partnerships, smart fee setups, and a deep understanding of what modern shoppers want. And, as the Sezzle platform continues to evolve, it’s likely to keep growing right alongside its users.

FAQs

No, Sezzle’s Pay in 2 and Pay in 4 plans are interest-free. Only the Pay Monthly option includes interest, with APRs up to 34.99%.

You may be charged a late fee of up to $15 and potentially a failed payment fee of up to $5. Repeated issues can affect your credit if enrolled in Sezzle Up.

Limits start low and increase as users make on-time payments. Sezzle uses purchase history and account behavior to manage risk.

Sezzle isn’t available everywhere, but there’s still a lengthy list of supported stores. You can use Sezzle at partnered retailers or anywhere Visa is accepted using the Sezzle Virtual Card, depending on your plan.

Not necessarily. Sezzle runs a soft credit check, which doesn’t harm your score. In fact, if you enroll in Sezzle Up and pay on time, it can actually help build your credit history.