I’ve had that moment where a flight looks fine at first, and then the total at checkout makes me stop in my virtual tracks.

That’s usually when fly now, pay later starts sounding a lot more appealing.

If you need to lock in a trip before prices go up again, splitting the cost can seem like the easiest way to do so. The problem is that these offers are usually sold on convenience, not clarity. The low payment gets all the attention. The terms, fees, and approval details?

They usually don’t.

So, I dug into how these plans usually work, what “no credit check” can actually mean, and where the real cost tends to creep in. Here’s what actually matters before you put a flight on a payment plan.

Key Takeaways

- Know What “No Credit Check” Really Means: It doesn’t always mean no review at all, so it’s worth reading the terms before you book.

- Small Payments Can Still Add Up: Breaking up the cost can help, but the total price still matters.

- Checkout Language Can Be Misleading: Terms like flex pay can sound simple, but you’re still agreeing to a real repayment schedule.

- Fees Matter More Than the Sales Pitch: Interest, late charges, and other add-ons can make a flight cost more than expected.

- The Best Plan Fits Your Budget: A payment option only helps if the due dates and amounts actually work for you.

How These Buy Now, Pay Later Travel Plans Usually Work

In most cases, the setup is pretty straightforward:

- You pick your trip and review the purchase details.

- You choose one of the payment options offered at checkout.

- You may make a down payment right away.

- The rest is split into installment payments spread out over time.

- Future charges are automatically deducted from your payment method.

Some travel sites call this a payment plan. Others use terms like monthly financing or flex pay. However it’s labeled, the basic idea is the same: instead of covering the whole purchase price in one shot, you break it up.

You may also see fixed monthly payments, monthly installments, or fixed monthly installments, depending on the provider and the schedule attached to the booking

The Way I Book Flights With BNPL

Before we get into specific airline partnerships, I want to share something that’s actually worked better for me in real life.

Most airlines will accept a BNPL virtual card at checkout. That means you’re not limited to whatever pay-over-time option the airline shows—you can bring your own.

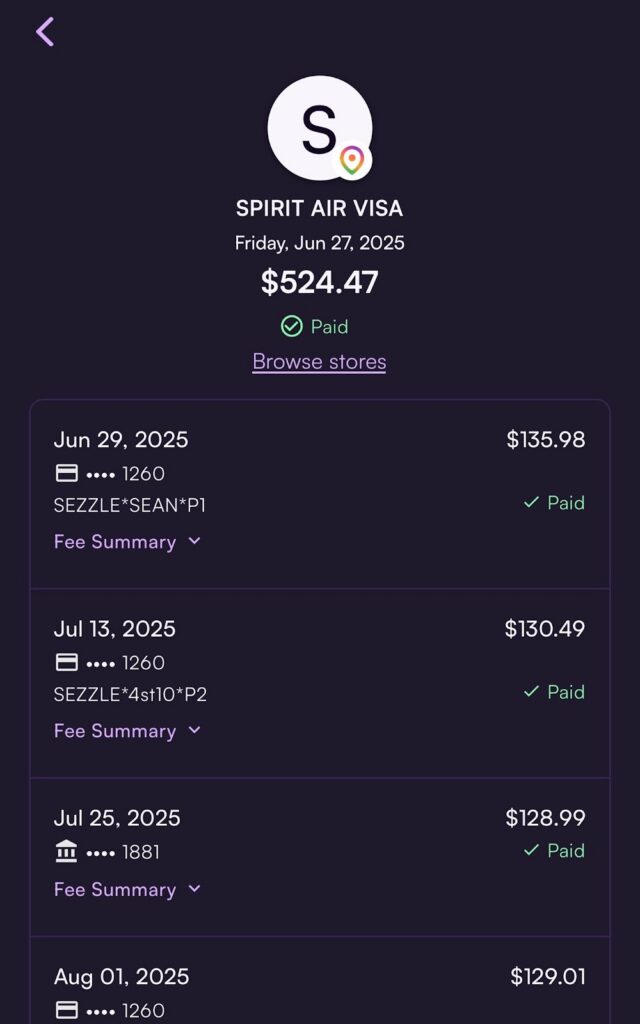

I’ve done this using Sezzle.

In this case, I booked a flight through Spirit, and instead of using a built-in financing option, I went through the Sezzle app first. You request the amount you need, and it generates a virtual card for that purchase.

One small thing I always do: I request about a dollar more than the total, just to make sure it covers taxes or any last-minute changes in price.

Then I take that virtual card number, go back to the airline’s checkout page, and enter it like a normal payment method.

From the airline’s side, it just looks like a regular card purchase. On my end, Sezzle splits it into payments.

That’s exactly what you’re seeing here—a flight purchase broken into smaller payments over time.

What I like about this approach is how flexible it is. I don’t have to worry about whether a specific airline partners with a BNPL provider or compare a bunch of financing offers. I can book the exact flight I want and still use a payment plan I already trust.

It’s one of those things that’s not super obvious until you try it—but once you do, it makes booking a lot easier.

Which Airlines Offer BNPL for Flights?

Let’s talk about the airlines that might work with your BNPL plans.

- United Airlines: United says its partner Flex Pay lets travelers book trips with monthly installments.

- Southwest Airlines: Southwest offers Flex Pay, allowing travelers to spread the cost over fixed monthly payments.

- Alaska Airlines: Alaska also offers Flex Pay and walks travelers through the process of using it at checkout.

- Spirit Airlines: Spirit has a Flex Pay support page and says travelers can fly before the balance is fully paid off, as long as there’s enough time before departure for processing.

- American Airlines: American says travelers can use Affirm for flights and seats, and eligible Citi / AAdvantage cardmembers can also use Citi Flex Pay at checkout.

- Delta Airlines: Delta Vacations offers Affirm for travel, so that’s the clearest official Delta-branded pay-over-time option I found.

Which BNPL Providers You’re Most Likely to See

Now, let’s take a look at the top BNPL providers for flight bookings.

- Flex Pay: This is the big one for airline bookings right now. Southwest and Alaska both describe it as a way to split travel into fixed monthly installments, and Upgrade notes that Flex Pay loans may require a down payment, can range from 0% to 36% APR, and aren’t available to everyone.

- Affirm: American uses Affirm for flights and seats, and Delta Vacations uses it for travel bookings paid over time.

- Citi Flex Pay: This one is more limited, but it still matters. American offers it to eligible Citi / AAdvantage cardmembers as a way to split a purchase into fixed monthly payments.

- Sezzle: Sezzle has a dedicated flights/travel category and lets shoppers use a Sezzle virtual card for travel purchases, including brands like Expedia, Priceline, Travelocity, CheapOair, Orbitz, and even airline listings like American Airlines and Southwest.

If you’re trying to figure out who actually offers this, the bigger thing to watch is the BNPL provider, not just the airline.

Sezzle is worth knowing about here because even when it isn’t the default BNPL button on an airline’s site, it can still be a practical way to split up flight costs through the Sezzle app or virtual card.

What “No Credit Check” Usually Means

This is where people should slow down a little.

When a site says there’s no credit check, that doesn’t always mean there’s no review happening at all. It usually means the company is using a different screening process, or that outside lending partners are involved somewhere behind the scenes.

It also means not everyone will see the same offer. Some travelers may get access to more financing options, while others may see fewer choices or different terms. In some cases, credit approval still comes into play, even if the checkout page leads with softer language.

That’s why I wouldn’t assume the headline tells the whole story. The actual terms matter a lot more than the marketing.

The Language You’ll See at Checkout

Travel brands are very good at making all of this sound easy.

You might see buy now, pay later on one site, while another leans into flexible payment options. Some pages use phrases like “choose flex pay,” which makes the whole thing feel pretty casual.

And to be fair, sometimes it is really that simple.

But that kind of wording can also make it feel less serious than it is. You’re still agreeing to scheduled payments tied to a travel purchase, and that deserves a closer look before you move too fast.

What To Check Before You Book

Before you use one of these plans, these are the main things worth checking:

- The schedule

Look at the payment dates and make sure they work with your budget, especially if several charges will hit before the departure date. - The total cost

Some plans are interest-free if everything is paid on time. Others may include interest charges, interest rates, late fees, or extra fees that make the trip cost more than expected. - The number of charges left

Check how many remaining payments you’ll still owe after checkout, so nothing sneaks up on you later. - The booking itself

Make sure the flight ticket details look right, especially if you’re trying to book flights for a time-sensitive trip. - What happens if something changes

If anything feels unclear, it’s worth contacting the customer service team before you commit.

A Few Red Flags Worth Watching

Some plans are fine. Some just look better than they really are.

Here are a few things I’d watch for:

- Hidden fees that only show up deep in the terms

- Repayment windows that feel too tight for real life

- Vague wording around monthly payments

- Confusing differences between financing options and regular checkout

- Added costs that make a decent deal feel less useful

It’s also worth remembering that while travel doesn’t come with shipping costs, that doesn’t mean the final number is always as clean as it first looks. If the pricing page feels fuzzy, I’d take that as a sign to pause.

When It Can Actually Make Sense

Used carefully, these plans can be helpful.

If you need to lock in international flights for something important, splitting up the cost may be easier than paying everything at once. The same goes for later flights you want to grab before the fare changes again.

That said, I think these work best for thoughtful purchases, not impulse bookings. A payment tool can help with timing, but it doesn’t magically make a trip affordable if the numbers already feel tight. If it makes sense for you, though, you can also book hotels using buy now, pay later to really spread out travel costs.

The Bottom Line

Fly now, pay later can be a useful option when the structure is clear, and the cost still makes sense once the excitement of booking wears off.

The main thing is to read carefully, know what you’re agreeing to, and make sure the plan fits your budget before you hit confirm.

FAQs

Sometimes, yes. Some travel payment providers advertise no credit check, but that doesn’t always mean there’s no approval process at all.

No. Some are interest-free if you pay on time, while others may include interest or extra fees depending on the provider.

Not always. Some plans require an upfront payment, while others split the full cost into scheduled payments.

Yes, in many cases. It depends on the travel site, the provider, and the total cost of the booking.

Look at the total cost, payment dates, fees, and what happens if you miss a payment. That’s usually where the biggest surprises show up.