BNPL has a way of shrinking a price in your head.

A purchase feels a lot different when it’s framed as four smaller payments…

Especially now.

A recent LendingTree survey found 41% of BNPL users paid late on at least one loan in the past year. For something that’s supposed to make paying easier, that’s a pretty telling number.

Afterpay is one of the biggest names in the space, so I looked at the app and what it’s actually like to rely on: how the payment plans work, what happens if something goes sideways, and whether it feels genuinely helpful or just convenient in the moment.

Let’s break it down.

Afterpay Overview

Afterpay feels like one of the more straightforward BNPL apps at first glance. The main appeal is simple: you can split a purchase into smaller payments instead of paying the full amount upfront, which may be helpful when you need something now but don’t want to drain your account all at once.

What I think Afterpay does well is keep the core idea easy to understand. For most purchases, it’s still centered around Pay in 4. More recently, it’s also added monthly payment options for some purchases, but the biggest draw is still that quick, familiar split-payment setup people already recognize at checkout.

To me, Afterpay works best as a cash-flow tool, not a budgeting solution. It could be useful when you’re buying something planned or necessary and just want a little more room in your checking account. At the same time, the app leans heavily into shopping, so it might be tougher to keep impulse spending in check. That’s kind of the theme with Afterpay overall: it’s easy, convenient, and useful in the right situation, but it can also make spending feel a little too easy.

Pros

✅ Simple Pay in 4 structure for standard purchases

✅ No finance charge on the standard installment agreement

✅ Available online and in-store

✅ Easy to track payments inside the app

Cons

❌ Pay in 4 can still trigger late fees and account pauses if you miss a payment

❌ The app is built to keep you shopping, not just tracking bills

❌ Spending limits and approvals can change, so it isn’t always predictable at checkout

My Personal Experience Using Afterpay Through Cash App

What’s interesting is that I didn’t actually go looking for Afterpay in the first place. I already use Cash App regularly for business and personal payments, especially when paying assistants or sending money quickly. Since Afterpay is now integrated into Cash App, I ended up trying it almost by accident.

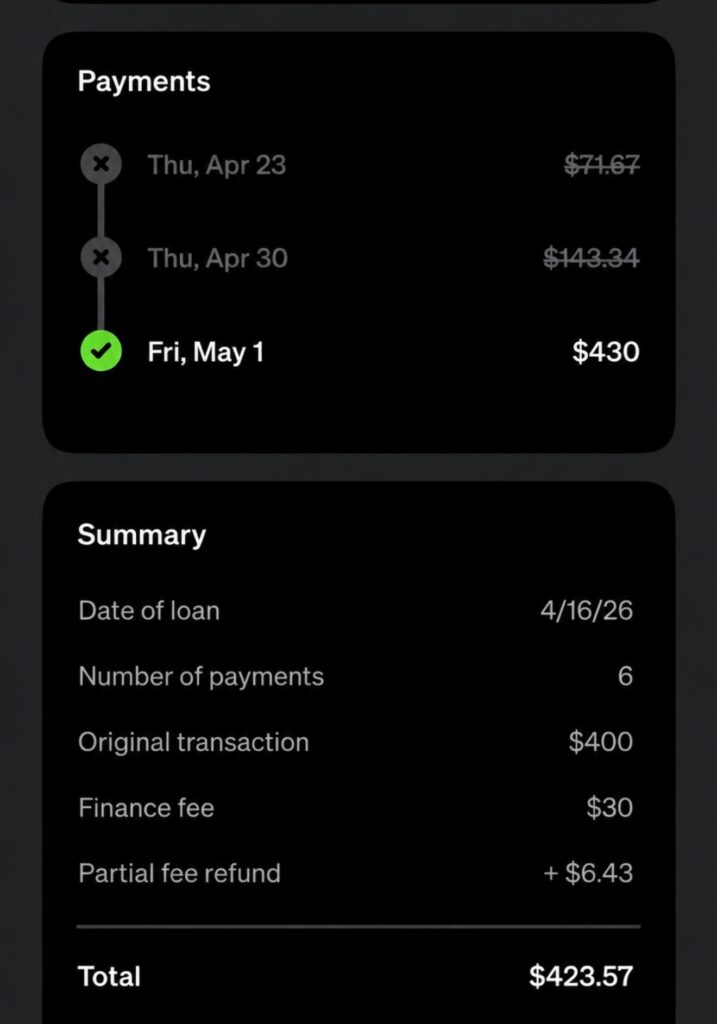

The feature first popped up after I made a purchase for about $423 and paid for it in full. Right afterward, Cash App gave me the option to essentially reverse the charge and split the purchase into six smaller payments through Afterpay instead. There was about a $30 fee attached, which normally would have made me pass on it immediately, but I was curious about how the experience actually worked in real life.

The setup process was simple, and the payment schedule was easy to follow inside the app. What surprised me most was what happened when I paid the balance off early. Afterpay refunded me approximately $7 back from the financing cost, which I honestly wasn’t expecting.

That experience made me look at Afterpay a little differently. I still wouldn’t use it for random impulse spending, and I definitely noticed how easy these payment apps can make larger purchases, from using BNPL for tires to plane tickets, feel smaller than they really are. But as a built-in feature inside Cash App, it was convenient and surprisingly frictionless to test out.

Payment Plans And Flexibility

For most people, Afterpay still feels like a Pay in 4 tool first. Pay a portion upfront, then the remaining payments are auto-drafted from the buyer’s account every two weeks. That rhythm is easy to understand, which is part of the appeal. There’s not much mental math involved.

If you’re looking at a $500 cart under standard Pay in 4, you’ll know exactly what you’re dealing with: $125 today, then $125 every two weeks until it’s done. That’s smooth. Predictable. Easy to calendar. But the same structure also becomes rigid fast if payday timing shifts or you stack three or four BNPL orders at once.

That’s the real Afterpay tradeoff to me. It’s simple, but not especially forgiving. If you were to miss a payment, your account can be paused, you may incur late fees, and your spending limit may drop. That makes the tool feel good when life is stable—and much worse when it isn’t.

Fees, Interest, And Transparency

This is where Afterpay still has a strong case. Standard Afterpay purchases carry no finance charges and no interest payments. Basically, if you stick to the plan, everything will work out.

But “interest-free” only tells part of the story now. Afterpay’s Pay Monthly option is a separate installment loan product, with APRs ranging from 0.00% to 35.99% depending on eligibility and merchant, though the help page says there are no late fees or origination fees on Pay Monthly. So the service is no longer just one thing. It has a genuinely low-friction short-term version and a more traditional financing version sitting beside it.

That’s why Afterpay feels relatively transparent to me in its standard form. With plain Pay in 4, the cost story is straightforward. I’d be wary about moving into longer-term financing, though; it stops being the simple no-interest button people tend to associate with the brand.

App Design And Ease Of Use

Afterpay’s app still looks more like a shopping destination than a budgeting tool. Its U.S. site and App Store listing emphasize curated roundups, exclusive deals, gift cards, and discovering brands in the app, right alongside payment management. That’s useful if you like the shopping experience. It’s less helpful if you open the app to stay organized and leave.

On the practical side, the current setup looks pretty smooth. Afterpay says first-time customers complete a quick registration, returning customers log in, and the app lets me manage payments and review upcoming orders. Support is app-first, but the help center also lists 24/7 digital support and a U.S. phone number.

My overall read is that the app worked the best when you’re disciplined. It’s clean enough to use, but it did feel like it was explicitly designed to keep you in the app, spending. So yes, it functions well. No, I wouldn’t confuse that with being especially good for self-control.

Is Afterpay Right for You?

Choose Afterpay If…

- You want a simple Pay in 4 plan without revolving credit card interest.

- You’re buying something you’d purchase anyway and just want to spread the hit across six weeks.

- You like a shopping app that also keeps your due dates visible.

Don’t Choose Afterpay If…

- You need lots of wiggle room to move payment dates around.

- You already lose track of small recurring payments and don’t want another one in the mix.

Final Verdict

Afterpay works best when you already know you can afford the purchase and just want a little more room in your budget. It’s simple, easy to use, and useful for splitting planned expenses into smaller payments.

The downside is that it didn’t give me much flexibility. If you miss a due date or need more control over your payment schedule, it can get stressful fast. For me, Afterpay is fine for occasional, planned purchases; if you want something with more tools, options, and control, I’d recommend Sezzle.

FAQs

For standard Pay in 4 purchases, there are no finance charges and no interest payments. The newer Pay Monthly option is different and can carry APR-based pricing.

It can. Missed payments may lead to late fees, an account pause, and a lower spending limit on future purchases.

Pay Monthly eligibility requires a soft credit check with no impact on your credit profile. Its standard Pay in 4 flow is still marketed more like a quick checkout approval experience.

Not really in the way Sezzle Up or current Affirm reporting might appeal to someone focused on credit visibility.

It varies, but I think using Sezzle is usually better for most people. It offers greater flexibility, better payment tools, and a more useful overall experience, while Afterpay feels more basic and much less forgiving.