Sometimes the problem isn’t the purchase — it’s the timing. I’ve had moments where I needed to buy something immediately, but didn’t want to throw it on a credit card and deal with interest later.

That’s what made me try Sezzle.

After using it for real purchases, I realized it was more than just another pay-in-4 app. In this Sezzle review, I’ll share my personal experience using the app, what stood out to me, and whether I think it’s actually worth using.

Sezzle Overview

Sezzle is a buy now, pay later app designed around short-term installment plans. Its core option is Pay in 4, but it also offers Pay in 2, Pay in 5, Pay in Full, and monthly financing on select purchases. On top of that, Sezzle has added features like Sezzle Up for optional credit reporting, plus Sezzle Premium and Sezzle Anywhere for broader access and extra perks.

My experience with Sezzle was positive overall because it felt simple in the ways that matter. I could quickly see my payment schedule, track purchases without any confusion, and use the app without feeling like I was fighting the interface. That made it feel less like a gimmicky shopping app and more like a tool I could actually use to stay organized.

Pros

✅ Easy to Understand: The short-term plans are simple and don’t require a bunch of math to follow.

✅ Helpful Payment Visibility: The app keeps upcoming payments and order details easy to find.

✅ Optional Credit Building: Sezzle Up lets you opt in to credit reporting instead of forcing it on everyone.

✅ Reschedule Feature: Some qualifying orders can be moved, which makes the app feel more forgiving than a rigid autopay setup.

✅ Broader Shopping Access: Sezzle Anywhere is a subscription I love because I can open up use beyond regular partner checkout pages.

Cons

❌ Fees Can Add Up: Sezzle can charge service fees, failed-payment fees, late-payment fees, rescheduling fees, and Late Saver fees, depending on your order.

❌ Best Extras Aren’t Fully Free: Some broader shopping and fee-waiver perks require Premium or Anywhere, which are paid subscriptions.

My Personal Experience Using Sezzle

I’ve used Sezzle several times when I wanted a little extra flexibility without taking on credit card interest or dealing with hidden fees. What I like most is that it gives me breathing room for unexpected purchases while still keeping payments manageable and predictable.

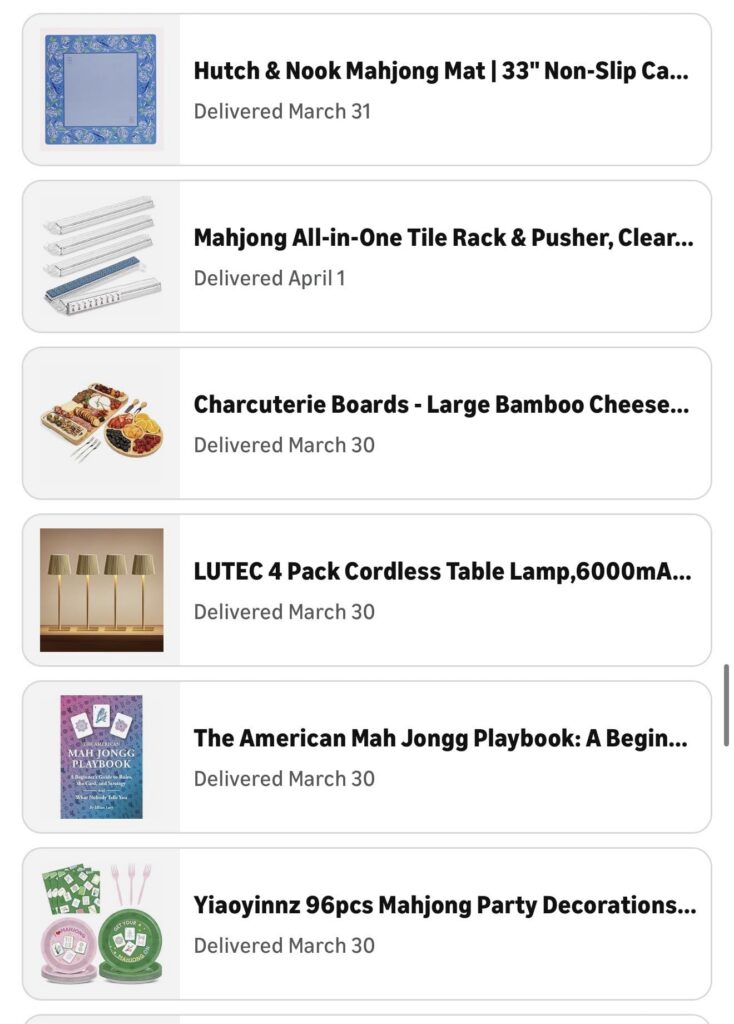

One situation where Sezzle really helped me was when I started a new business teaching people how to play American mahjong. As I was preparing for one of my events, I realized I needed additional supplies and materials at the last minute. The unexpected costs added up quickly, and I wanted a simple way to cover everything without disrupting my cash flow.

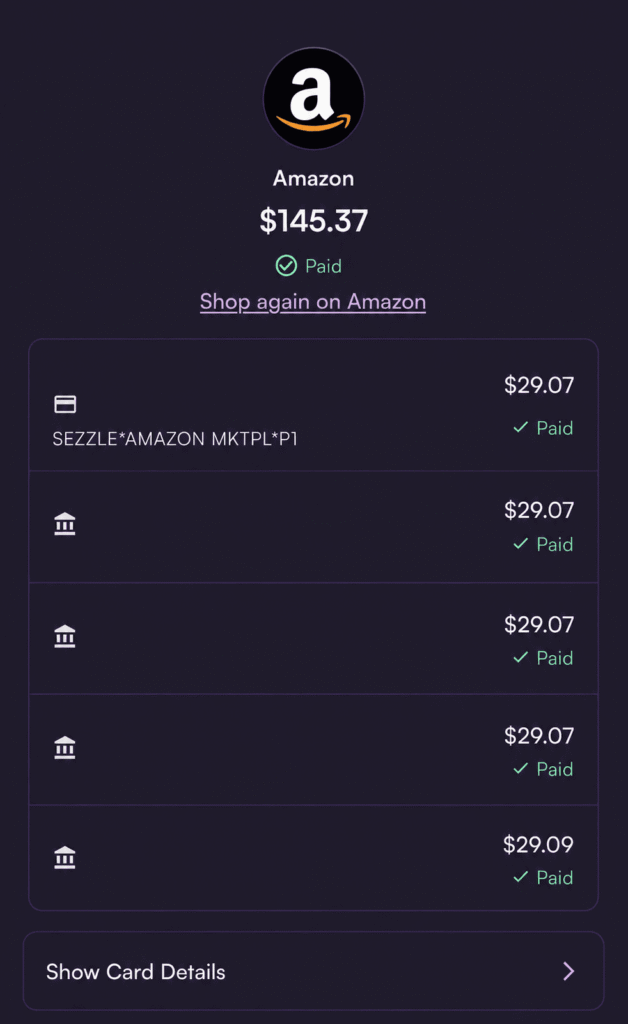

I used Sezzle for an Amazon BNPL purchase to get the extra items I needed for the event, and the process was incredibly easy. Because I have the Sezzle Anywhere subscription, I was able to pay the balance off quickly with zero interest and no extra fees. If I had decided to spread the payments out instead, they would have been less than $30 per week, which made the purchase feel much more manageable.

For me, Sezzle worked exactly the way I hoped it would: a convenient short-term payment option that gave me flexibility when unexpected business expenses came up, without creating long-term debt or expensive financing charges.

Payment Plans & Flexibility

Sezzle works best when you want to spread out a purchase without turning it into a long loan. The main short-term plans are Pay in 2, Pay in 4, and Pay in 5, and those are the options that make the most sense for everyday budgeting. If you’re looking at something bigger, Sezzle also has monthly financing on some purchases.

In real dollars, a $200 purchase on a four-payment plan breaks into four $50 payments. That may sound almost too obvious to mention, but it’s part of why Sezzle works. The math stays simple, and I never felt like I had to decode what I owed.

Flexibility is one of Sezzle’s better features. Qualifying orders can be rescheduled, and in some cases, payments can be moved more than once—though fees may apply depending on the order and your state. Premium and Anywhere also add one free reschedule per order as part of the membership perks.

From a mental-load standpoint, Sezzle felt lighter than I expected. I liked being able to open the app and immediately see what was due, what had already been paid, and what my next few weeks looked like. That made it feel more like a budgeting tool than a shopping trap. The overall experience was smooth once I got past an old-account login issue tied to a previous phone number. That part was annoying, but support helped clear it up quickly.

Fees, Interest & Transparency

This is where I think people need to slow down and pay attention. Sezzle’s short-term plans are marketed as interest-free, and that part is true when you stay on track. But “interest-free” does not mean “free.” Service fees can apply to some orders, especially on certain virtual card uses, and Sezzle also charges failed payment fees, late payment fees, reschedule fees, and Late Saver fees in some situations.

Using the same $200 example, the best-case version is still just four clean payments of $50. But the cost starts changing once you add a fee-based virtual card, miss a payment, or push a date back more than the free allowance covers. That doesn’t make Sezzle deceptive, but it does mean the cheapest version of Sezzle is the disciplined version.

I do think Sezzle is fairly transparent about where those charges come from. The fee categories are laid out clearly in its help materials, and the service-fee language is tied to specific use cases instead of being buried in vague copy. That said, the app becomes a lot more attractive when you don’t need the paid extras. Premium and Anywhere can waive some service fees and add perks, but they also turn a simple BNPL tool into something closer to a subscription product.

App Design & Ease Of Use

Once I got into the app, Sezzle was easy to navigate. The layout is clean, and the parts I cared about most, like due dates, active orders, and spending access, were easy to find. I didn’t feel like I had to dig through glossy shopping clutter just to check my payment schedule.

The biggest setup quirk for me was account access. I had used Sezzle years ago with an old phone number, so getting back in was more annoying than I wanted it to be. But after support helped reset the old account, the rest of the experience felt smooth. That fix didn’t make me love the signup process, but it did leave me with a better impression of the support side.

The virtual card side is where Sezzle gets more layered. If you stick to normal partner checkout, the experience is simple. If you want wider flexibility, Sezzle Anywhere gives you a multi-use virtual card that can work online and in-store wherever Visa is accepted, with some exceptions. That’s useful, but it also means the most flexible version of Sezzle is not the basic free version.

My overall user-experience summary is pretty simple: Sezzle feels reliable, calm, and easy to manage when you use it for what it’s best at, which is short-term purchase splitting. It starts to feel less elegant when you layer on memberships, service fees, or virtual-card workarounds.

Is Sezzle Right for You?

Choose Sezzle if…

- You want simple short-term installment plans

- You like having one place to track what’s due

- You want optional credit building through Sezzle Up

Don’t choose Sezzle if…

- You know you’ll need a lot of payment flexibility

- You want the cleanest fee structure possible

Final Verdict

After using Sezzle and digging into how it works, I came away liking it (and I still use it today!).

The app is easy to use, the payment plans are simple, and the overall experience feels a lot more manageable than putting everyday purchases on a high-interest credit card. I also like that Sezzle Up gives users a chance to turn responsible payments into something more useful over time.

Overall, I think Sezzle is a strong BNPL option for people who want flexibility without a lot of confusion. It works especially well for everyday purchases, short-term budgeting, and anyone who likes having a clear payment schedule instead of a revolving balance hanging over them.

FAQs

Sezzle’s short-term plans, like Pay in 2, Pay in 4, and Pay in 5, are built as interest-free options, but monthly financing can carry interest depending on the purchase and offer.

Yes. Service fees, late payment fees, failed payment fees, reschedule fees, and Late Saver fees can all come into play depending on how you use the app and whether your payments stay on track.

Sezzle can build credit, but only if you opt into Sezzle Up. That program reports your payment history to credit bureaus, which means on-time payments can help, and delinquent payments can hurt.

Yes, but the broader in-store experience depends on Sezzle Anywhere and the multi-use virtual card through Apple Pay or Google Pay. Basic partner checkout is still the simpler path.

I think it is if you want a short-term budgeting tool and you’re disciplined about payments. I wouldn’t use it if you already know you’ll be leaning on reschedules, extra fees, or paid memberships just to make it work.