30% of Americans fall below the threshold for a good credit score.

But a good credit score isn’t really negotiable.

You need a good score for things like getting a loan, buying a home, renting an apartment, and sometimes even getting a job. With BNPL on the rise, a lot of users are wondering: Does Sezzle build credit history?

As a long-term user who’s done the real research to get to the bottom of it, here’s what you need to know about using Sezzle in a way that doesn’t hurt your credit.

Key Takeaways

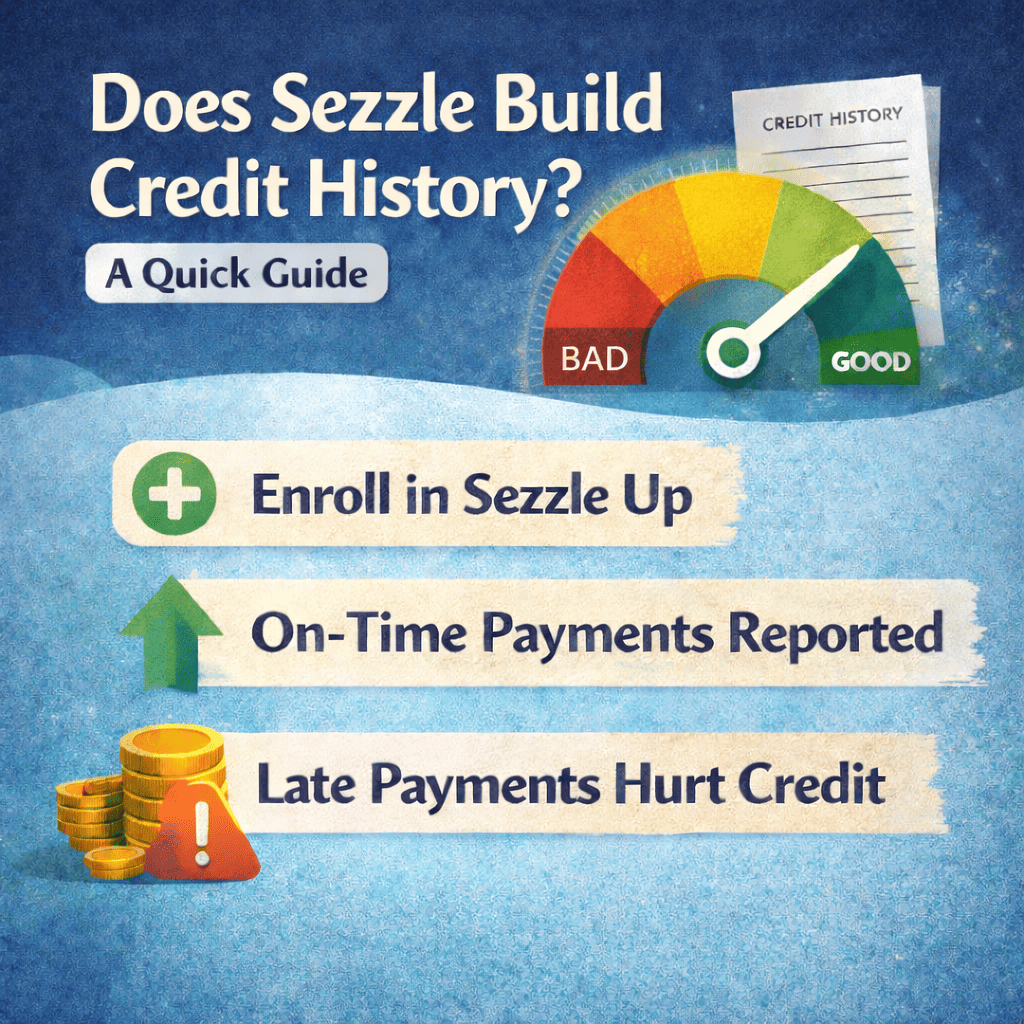

- No Default Credit Building: Sezzle does not build credit history automatically unless you enroll in Sezzle Up.

- Standard Purchases Stay Off Reports: Regular installment purchases usually do not appear on your credit reports by default.

- Sezzle Up Can Help: Sezzle Up reports payment history, which can help build credit for users with limited or newer credit files.

- Late Payments Can Hurt: Missed or late payments reported through Sezzle Up can negatively affect your credit.

- Check Before Assuming: To confirm reporting, review the Sezzle Up section in the app and check your credit reports.

How Sezzle Works And Why Credit Reporting Is Not Automatic

Sezzle’s standard setup is legit and simple: you split a purchase into installments, usually four payments over several weeks. For most users, that basic arrangement does not automatically get reported to the major credit bureaus.

That means regular Sezzle use typically stays off your credit reports. Sezzle may use a soft credit check when you sign up, which generally doesn’t affect your credit file. So if you’re asking whether everyday Sezzle purchases build credit history on their own, the answer is usually no. You have to take an extra step before payment activity becomes part of your reported borrowing record.

When Sezzle Can Help Build Credit History

Sezzle can help build credit history when you enroll in Sezzle Up, its optional reporting feature. That’s the part that changes Sezzle from a simple installment tool into something that may contribute to your documented payment track record.

This can be especially useful for people with thin credit files, students, newer borrowers, or anyone who hasn’t had many accounts reported before. Based on Sezzle’s published guidance, enrollment generally requires paying off one order on time and in full, linking a bank account for scheduled payments, and verifying personal information, including a valid Social Security number.

How Sezzle Up Changes What Gets Reported

Once you’re enrolled, Sezzle can report your payment history to credit bureaus monthly. In the app, reported months may appear as “Current” for on-time payments or “Not Current” if there are delinquencies. Sezzle says it can take up to 60 days from your first eligible order after sign-up for the account to appear on your credit report.

A practical detail matters here: not every transaction is necessarily included. For example, pay-in-full purchases generally aren’t the focus of credit reporting, while eligible installment activity is. So if your goal is to build credit history with Sezzle, you need the right program and the right type of repayment activity.

| Standard Sezzle | Sezzle Up |

|---|---|

| Regular payments are usually not reported | Eligible payment history can be reported |

| Does not build credit by default | May help build credit with on-time payments |

| Basic installment setup | Optional reporting feature |

| Missed payments may still lead to fees or collections | Late payments can hurt your credit if reported |

How To Check Whether Sezzle Is Showing On Your Credit Reports

To check whether Sezzle is showing on your credit reports:

- Open the Sezzle app and go to Account

- Look for Sezzle Up under the Benefits section

- Check whether recent months are marked Current or Not Current

- Review your credit reports from the major bureaus

- Wait up to 60 days after your first qualifying order before assuming nothing was reported

A good habit is to compare both sources: Sezzle’s in-app reporting status and your bureau reports. That gives you the clearest picture.

Sezzle vs. Other Buy Now, Pay Later Services

Compared with other buy now, pay later companies, Sezzle does a good job of making its credit-building path clear. Not every BNPL purchase automatically helps build credit history, and Sezzle is upfront about that. In most cases, you’ll need Sezzle Up for payment reporting to apply.

That clarity is useful, especially as BNPL repayment behavior becomes more visible in newer credit scoring models. Some competitors report selectively or tie reporting to certain loan products, but Sezzle’s approach is easier to understand: opt into the right feature, make on-time payments, and you have a more defined path.

That’s the biggest advantage. Sezzle gives shoppers a straightforward way to use BNPL while also understanding when credit reporting may come into play. As long as you read the terms and stay on schedule, the setup feels transparent and manageable.

Final Verdict

So, does Sezzle build credit history?

Yes, when you enroll in Sezzle Up and make eligible payments on time.

That makes Sezzle a useful option if you want BNPL with a clearer credit-building path. Standard Sezzle is mainly a payment-splitting tool, but Sezzle Up adds the potential benefit of documented on-time payment activity. Used consistently, it can be a simple way to make everyday repayment behavior count for more.

Frequently Asked Questions

No, standard Sezzle use does not report to credit bureaus and does not build credit history automatically. Only enrolling in Sezzle Up and making eligible payments on time can help build credit history.

Sezzle Up is an optional program that reports your monthly payment history to major credit bureaus. On-time installment payments through Sezzle Up can establish or strengthen your credit record, especially if you have a thin credit file.

To enroll in Sezzle Up, you must pay off one order on time and in full, link a bank account for scheduled payments, and verify your personal information, including providing a valid Social Security number.

Yes, if enrolled in Sezzle Up, late or missed payments can be reported as delinquencies, which may significantly lower your credit score and impact your future borrowing ability.

It can take up to 60 days after your first eligible order following Sezzle Up enrollment for your account activity to appear on your credit report.