Buy now, pay later is everywhere now. You see it at checkout for clothes, electronics, travel, and even everyday basics. The pitch is simple: get what you need today and split the cost into smaller payments over time.

That convenience is a big reason BNPL has taken off, with nearly 100 million users in America alone. But the easy checkout experience can hide the fact that not all buy now, pay later plans work the same way. Some are interest-free. Some come with fees. Some can be helpful budgeting tools, while others can make overspending a little too easy.

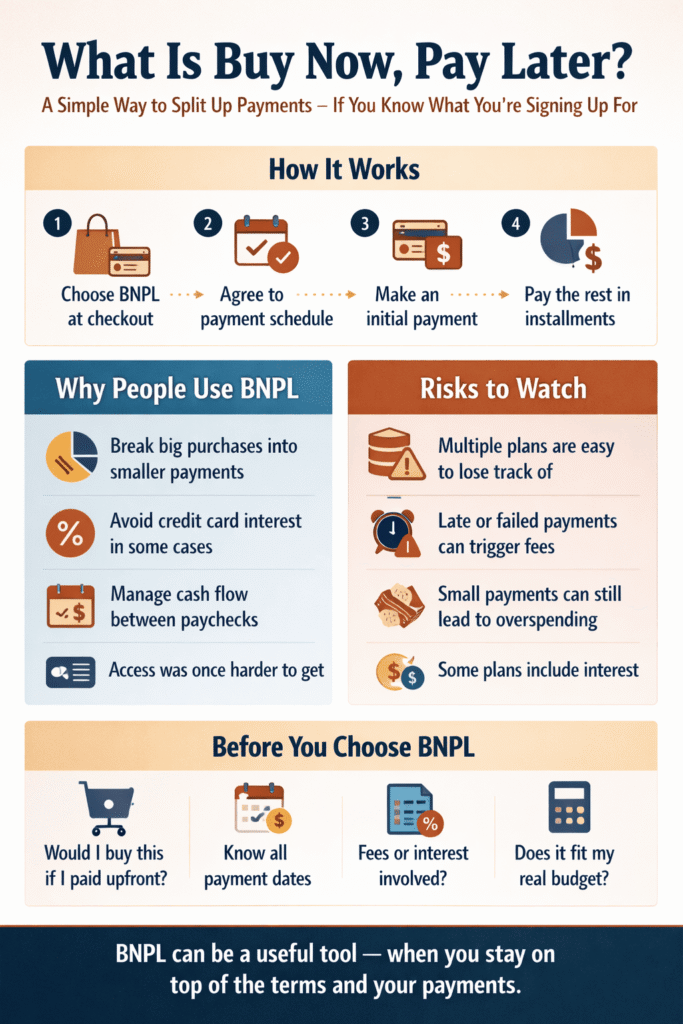

So what is buy now, pay later, really? Here’s how it works, why people use it, and what to watch before you choose it at checkout.

Key Takeaways

- It Splits Up Payments: Buy now, pay later lets shoppers break a purchase into smaller installments instead of paying the full amount upfront.

- Not All Plans Work The Same: Some BNPL options are interest-free, while others may include fees or longer-term financing charges.

- It Can Help With Flexibility: BNPL can make purchases easier to manage by spreading costs out over time.

- Small Payments Still Add Up: One of the biggest risks is losing track of multiple plans and overspending because each payment feels small.

- The Terms Matter: Before using BNPL, it’s important to check payment dates, fees, interest, and the total cost of the purchase.

Defining Buy Now, Pay Later

Buy now, pay later, often shortened to BNPL, is a payment option that lets you split a purchase into smaller installments over time.

Instead of paying the full price upfront, you agree to make a series of payments on a set schedule. In many cases, that schedule is short. A common example is paying in four installments over several weeks.

That’s what makes BNPL appealing. It breaks a bigger payment into smaller pieces that may feel more manageable.

Why People Use It

For a lot of shoppers, the appeal comes down to one thing: flexibility.

Paying $25 four times can feel easier than paying $100 all at once, even if the total cost ends up being the same. That can be helpful if you’re trying to manage cash flow, line up expenses with paydays, or avoid putting a purchase on a high-interest credit card.

Some of the most common reasons people use BNPL include:

- Spreading out the cost of a purchase

- Making checkout feel easier

- Avoiding credit card interest in some cases

- Managing short-term budget pressure

- Buying something necessary before the next paycheck

I’ve used buy now, pay later quite a few times myself, and I understand the appeal. In my experience, Sezzle has been one of the more useful options, especially because of its Anywhere program. It gives you a bit more flexibility in where you can use it, and I’ve been able to apply interest-free payment plans to things like travel and trips, which can make a bigger expense feel a lot more manageable. Like anything, it works best when you go into it with a plan, but used that way, it can be a helpful tool.

How Buy Now, Pay Later Works

The exact setup depends on the provider, but the basic process usually looks like this:

- You choose a buy now, pay later option at checkout.

- The purchase is approved based on the provider’s criteria.

- You make an initial payment or agree to a payment plan.

- The remaining balance is collected in installments over time.

In many cases, the payments are automatic, which means the money comes out of your linked debit card, credit card, or bank account on scheduled dates.

That convenience is part of the appeal. It also means you need to know when those payments are coming.

What Buy Now, Pay Later Looks Like in Real Life

In practice, BNPL often shows up in one of two forms.

Short-Term Installments

This is the version most people think of first.

You buy something today and split the total into a few smaller payments, often over six weeks or so. For example, a $560 plane ticket might be split into four payments of $140. Instead of paying the full amount upfront, you pay the first installment at checkout and the rest over time.

These plans are often marketed as interest-free, though that does not always mean free of all fees.

This type of BNPL is usually used for smaller purchases like clothing, beauty products, electronics, or even something like a last-minute trip.

Longer-Term Financing

Some BNPL providers also offer longer monthly payment plans for larger purchases.

For example, a $1,000 Airbnb stay might be spread out over several months instead of a few weeks. That can make a bigger expense feel more manageable, but it often works more like traditional financing.

Unlike short-term plans, these longer options may include interest. Depending on the provider, rates can be fairly high, sometimes reaching up to around 30% in certain cases.

That setup usually comes with different approval requirements and disclosures, which is why it can feel closer to a loan than a simple payment split.

This is one reason BNPL can be confusing. People use one phrase to describe products that may work pretty differently depending on the purchase and the provider.

Is Buy Now, Pay Later the Same as a Credit Card?

No. Both let you buy something now and pay later, but BNPL and credit cards work differently.

A credit card gives you a revolving line of credit. You can keep borrowing against it, carry a balance, and usually pay interest if you don’t pay the balance in full.

Buy now, pay later is usually tied to a single purchase. Instead of one ongoing credit line, you’re agreeing to a specific repayment plan for each transaction.

Here’s the quick comparison:

- Credit cards are ongoing and reusable

- BNPL plans are usually purchase-specific

- Credit cards often charge interest on carried balances

- BNPL plans may be interest-free, but some can include fees or interest depending on the terms

So no, they are not the same thing, even if they can feel similar at checkout.

Why BNPL Feels Easier Than It Is

This is where I think people can get tripped up. Buy now, pay later is designed to feel simple. The payments look small. The approval process can feel fast. The checkout experience often makes it seem low stakes.

But small payments add up.

A $40 payment here and a $25 payment there may not feel like much in the moment. But if you stack multiple BNPL plans at once, it gets surprisingly easy to lose track of what you owe and when it’s due.

That doesn’t mean BNPL is automatically a bad idea. It just means convenience can hide the real cost of overcommitting yourself.

The Main Benefits of Buy Now, Pay Later

Used carefully, BNPL can be genuinely helpful.

Here are some of the biggest advantages:

- Reduce upfront pressure on your budget

- Help you line up your payments with payday timing

- May offer interest-free short-term options

- Can be easier to access than some traditional credit products

- Gives shoppers more payment flexibility at checkout

That’s why many people like it. In the right situation, it can be a practical tool rather than a problem.

I think that’s the fairest way to look at it. BNPL is not inherently reckless. It just works best when you’re using it with a plan, not as a way to ignore what you can actually afford.

The Main Risks to Watch

The biggest risk with buy now, pay later is not always the product itself. Sometimes it’s the psychology.

Because the payments seem smaller, shoppers may feel more comfortable buying things they would not have paid for upfront. That can lead to overspending.

Other risks can include:

- Late fees

- Failed payment fees

- Interest on certain longer-term plans

- Overdraft fees from your bank if payments hit at the wrong time

- Juggling too many payment plans at once

This is why reading the terms matters. Not every BNPL provider works the same way, and not every plan carries the same costs.

Before You Use BNPL, Ask Yourself These Questions

If you’re thinking about using a buy now, pay later plan, it helps to pause and ask:

- Would I still buy this if I had to pay in full today?

- Do I know exactly when the payments will come out?

- Is this a short-term payment split or a financing plan?

- Are there any fees or interest involved?

- Am I using this for convenience, or because I’m already stretched too thin?

That last question matters most.

If BNPL is helping you manage cash flow responsibly, it can be useful. If it’s covering a gap you can’t realistically close, it can create more stress instead of less.

So, What Is Buy Now, Pay Later Really?

At its core, buy now, pay later is just a way to split up payments over time.

That’s the cleanest definition.

It can be a smart, convenient option when you understand the terms and stay on top of the schedule. It can also become a problem if you treat smaller payments like they don’t count or stack too many plans at once.

That’s why I think BNPL is best viewed as a tool. Not a scam. Not a miracle. Just a tool.

And like most financial tools, it can help or hurt depending on how you use it.

The Bottom Line

Buy now, pay later is a payment option that lets shoppers make a purchase immediately and repay the cost in smaller installments over time.

That can make purchases feel more manageable, especially with short-term payment plans. But not all BNPL options work the same way. Some are interest-free, some include fees, and some longer-term plans may involve interest.

If you use buy now, pay later thoughtfully, it can be a convenient way to spread out costs without relying on a traditional credit card. The key is understanding the terms, knowing your payment dates, and making sure the smaller payments still fit your real budget.

FAQs

Buy now, pay later is a payment option that lets you get an item now and repay the cost in smaller installments over time.

Not exactly. Credit cards are revolving credit lines, while BNPL is usually tied to one specific purchase and a fixed repayment schedule.

Sometimes. Many short-term plans are marketed as interest-free, but some BNPL options include fees or interest, especially for longer-term financing.

Yes, if you take on too many plans at once or miss payments. Smaller installments can feel manageable, but they can pile up quickly.

Most people use it for flexibility. It can make larger purchases feel easier to manage by spreading the cost over several payments.