By now, you’ve probably heard of Sezzle (or at least seen the “Select Sezzle” button sitting there at checkout). And if you’ve paused for a second wondering what Sezzle actually is and whether it’s legit, here’s your answer.

Sezzle started as a buy now, pay later platform that lets you split purchases into four interest-free payment plans. Simple enough. But since I used it to buy a plane ticket, it’s grown into something much bigger. Now there are multiple payment options, a virtual card you can use almost anywhere, in-app shopping tools, and even more on the way, including cash advances and cell phone service.

As a Sezzle user myself, let’s talk about what Sezzle really is—and whether it’s a smart choice for your real-life personal finance strategy.

Key Takeaways

- Flexible Payment Plans: Sezzle lets shoppers split purchases into Pay in 4 or Pay in 5 installment plans instead of paying the full amount upfront.

- Interest-Free Core Option: The standard Pay in 4 plan is interest-free, while some extended financing options may include a service fee or interest (especially if you pay monthly).

- No Hard Credit Checks: Sezzle uses a soft credit check for approval, so applying does not negatively impact your credit score.

- Online and In-Store Access: The Sezzle Virtual Card (not part of the payment card industry) can be added to Apple Pay or Google Pay, allowing you to use Sezzle for both online and in-store purchases where Visa is accepted.

- Expanding Financial Services: Sezzle is growing beyond traditional buy now, pay later products, with plans to introduce cash advances and cell phone service.

What Sezzle Offers Right Now

At a high level, Sezzle offers:

- Pay in 4—four interest-free payments over six weeks

- Pay in 5—a newer extended payment plan

- Sezzle Virtual Card—use Sezzle for online purchases almost anywhere Visa is accepted

- Instant approval with no hard credit check

- Optional credit reporting to build credit history

- In-app price comparison and shopping tools

- And soon—cell phone service and personal loans

Sezzle has evolved significantly since I used it to book a plane ticket, and its range of services is much broader than most shoppers expect. Plus, it’s building up to include even more features in the future, indicative of the service’s level of success.

What’s Next: Cell Phone Service and Cash Advances

Curious about what’s on deck for Sezzle? Currently, the company is expanding beyond installment payments, moving into features such as:

- Cell phone service offerings

- Cash advances

That signals a shift toward becoming a broader financial services platform rather than strictly a buy-now-pay-later company. Now, let’s get into the nitty-gritty: what using Sezzle is actually like, and how I used it to make plane tickets easier on my budget.

Pay in 4: The Classic Sezzle Payment Plan

The original Sezzle structure is simple.

When I chose Sezzle at checkout:

- I paid 25% of the purchase price as my first payment

- The remaining amount was split into three equal installments

- Payments are automatically scheduled every two weeks

- No interest is charged if you pay on time (so I had no interest)

It’s really that simple, and it looks the same for every consumer.

What Pay in 4 Looks Like in Real Life (My Spirit Airlines Experience)

Airfare prices have been anything but stable over the past several years. After dropping sharply in 2020, fares have surged before cooling again, making it harder for us to predict what we will pay from one season to the next. That kind of volatility can make travel budgeting more difficult, especially when ticket prices shift quickly.

This is where Sezzle comes in.

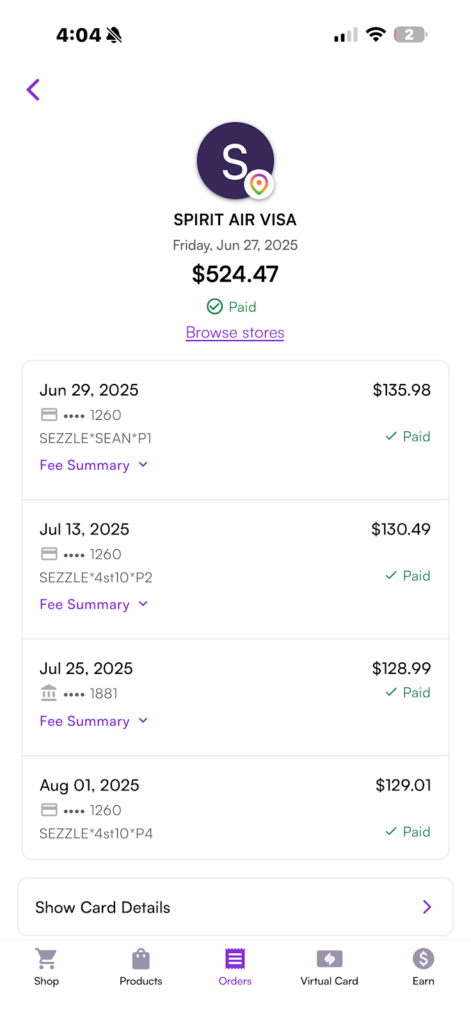

When I used Sezzle to buy a Spirit Airlines plane ticket, the total purchase price was $524.47.

Instead of paying the full total cost upfront, I selected Sezzle at checkout and split the purchase into installments.

Here’s how it broke down inside my Sezzle account:

- June 27, 2025: $135.98 (first payment)

- July 13, 2025: $130.49

- July 25, 2025: $128.99

- August 1, 2025: $129.01

Each payment was automatically scheduled and marked as paid once processed. I could see every installment inside the Sezzle app, along with a fee summary and confirmation that the payment cleared (read: it was a lot easier and more automatic than I expected it to be).

This gave me:

- A predictable payment schedule

- Transparency for and about each scheduled payment

- No confusion about how much I owed for each installment

- No revolving interest

Instead of one $524 charge hitting my bank account at once, the cost was spread out over several weeks in four interest-free installments.

That’s the core Sezzle model in action.

What This Shows About How Sezzle Works

Using my own purchase as an example makes a few things clear:

- You always see the full total cost upfront.

- Payments are split into equal or near-equal installments.

- The first payment happens immediately.

- The remaining amount is auto-drafted on scheduled dates.

- Everything is tracked inside the Sezzle app.

There’s no long-term loan structure, no minimum payment trap, and no compounding interest like traditional credit cards.

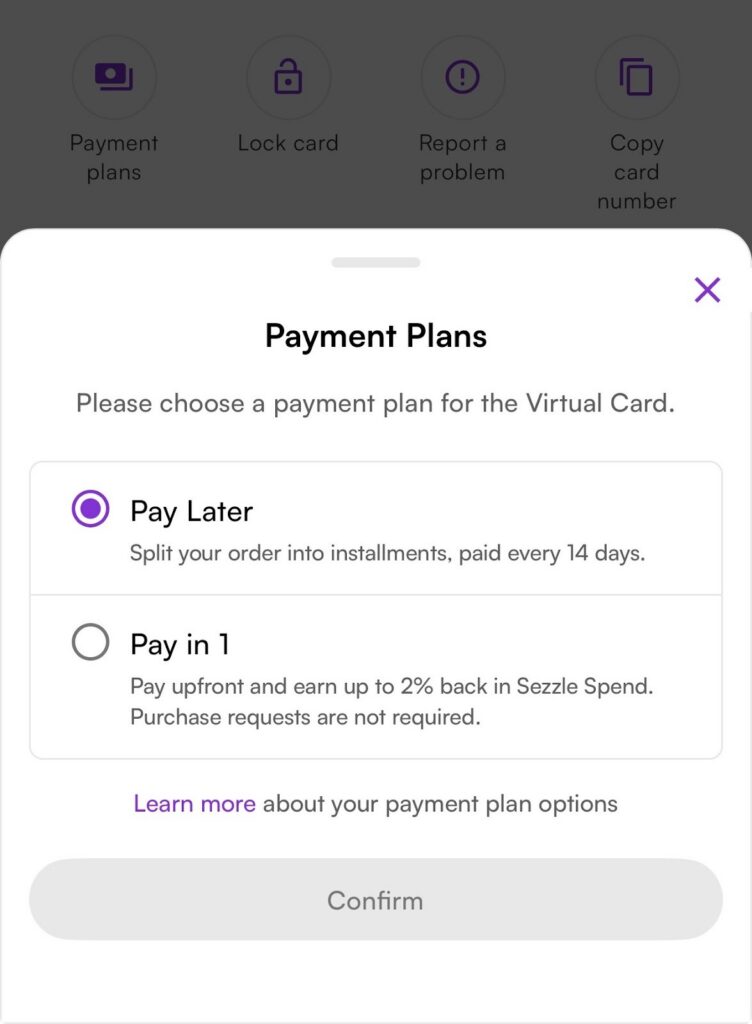

Pay in 5: More Flexibility for Larger Purchases

Sezzle’s newer Pay in 5 option extends that model.

Instead of four installments over six weeks, Pay in 5 leads to five scheduled payments over a longer timeline. That lowers each payment, giving consumers a little more room to breathe.

Pay in 5 can make sense for:

- Travel bookings

- High-ticket retail purchases

- Seasonal or holiday spending

- Added flexibility in your budget

Some extended pay-later loans may include a disclosed service fee depending on the Sezzle product and purchase price. You’ll always see the full total cost before confirming.

So, while standard Pay in 4 is interest-free, certain longer financing options may involve a fee (which is clearly shown at checkout).

Sezzle Virtual Card: Pay Later Anywhere

One of the biggest upgrades to the Sezzle platform is the Sezzle Virtual Card. Instead of being limited to participating in online stores, you can:

- Download the Sezzle app

- Set up your virtual card

- Add it to Apple Pay or Google Pay

- Use it in-store or online anywhere Visa is accepted (subject to approval)

This dramatically expands where Sezzle works. To me, this makes Sezzle more of a flexible payment option rather than just a niche checkout button.

How Sezzle Approval Works

One common question is whether Sezzle hurts your credit score.

Here’s how Sezzle works:

- Sezzle runs a soft credit check, not a hard inquiry

- A soft check does not impact your credit score

- Approval decisions are typically instant

- You only need a valid phone number and payment method (debit card, bank account, or credit card)

Because it avoids traditional hard credit checks, Sezzle appeals especially to young consumers or those cautious about traditional credit applications.

Fees, Late Payments, and What to Watch For

Sezzle does not charge interest on its standard Pay in 4 structure. However, it is not completely free.

If you have missed payments:

- You may run into late fees

- Your account could be temporarily restricted

- Several missed payments may limit future approvals

Some products may include a service fee, disclosed clearly before checkout.

Smarter Shopping Tools Inside the Sezzle App

Sezzle is positioning itself as more than just a pay-later button.

Inside the Sezzle app, users can:

- Track scheduled payments

- View outstanding balances

- Compare prices

- Discover exclusive brand perks

- Monitor payment history

- Manage their default payment method

It’s built to give users control over how they pay — not just access to financing. App ratings remain strong across major app stores, suggesting solid user experience and adoption.

Final Verdict: What Sezzle Is Really Becoming

Sezzle has grown far beyond simply splitting a purchase into four payments. Today, it offers Pay in 4 and Pay in 5 installment plans, a widely usable Virtual Card for online and in-store purchases, optional credit-building features, in-app shopping tools, and is expanding into products like cash advances and cell phone service. It’s positioning itself as a broader financial platform rather than just a buy now, pay later button.

For consumers who want structured, transparent payment plans without traditional credit card interest, Sezzle can be a practical alternative; however, like any financial tool, it works best when used intentionally and managed responsibly.

FAQs

No. Sezzle runs a soft credit check during approval, which does not impact your credit score. However, if you opt into credit reporting and repeatedly miss payments, that could affect your credit history.

Sezzle does not charge interest on its standard Pay in 4 plan. Some extended financing options, such as Pay in 5 or other loan products, may include a service fee that is disclosed before you confirm the purchase.

Pay in 5 allows you to split your purchase into five scheduled payments over a longer period than Pay in 4. This lowers each individual installment amount and can provide more flexibility for larger purchases.

You can use Sezzle at participating online stores, and through the Sezzle Virtual Card added to Apple Pay or Google Pay, you may be able to use it in-store anywhere Visa is accepted (subject to eligibility and approval).

Sezzle does not automatically report to credit bureaus. However, users can opt into credit reporting programs that may help build credit history if payments are made on time.