Gift cards are supposed to be the easy option…

But “easy” doesn’t always mean “cheap.”

That’s where buy-now, pay-later gift cards can start to sound appealing. If you’re spending more than you planned, breaking it up can seem like an easy fix.

The problem is that gift cards are a weird corner of BNPL. Some providers allow them. Some limit them. Some only work through certain apps or card setups, and the rules around fees, refunds, and restrictions are not always obvious.

I took a closer look at the main options, how they’re set up, and what I’d want to know before using BNPL for gift cards. Here’s what to keep in mind while you shop.

Key Takeaways

- Not Every Provider Allows Them: Some BNPL services let you buy gift cards, while others limit or block those purchases.

- Digital Usually Keeps It Simpler: E-gift cards are often easier to send and avoid extra shipping costs.

- Small Payments Can Be Misleading: A low monthly amount can still come with interest, fees, or stricter terms.

- Refund Rules Matter A Lot: Gift card purchases are often harder to cancel or return than regular orders.

- The Full Cost Still Counts: Before you check out, look at the total amount, not just the first payment.

Are Buy Now, Pay Later Gift Cards a Thing?

Yes, they are!

Right now, Klarna, Afterpay, Zip, and Sezzle all have consumer-facing ways to purchase gift cards, though they don’t all handle them the same way. Klarna has a dedicated gift card section and says gift cards can be purchased with pay later methods, Afterpay offers e-gift cards through its app, Zip sells gift cards through its app flow, and Sezzle has a gift-card page plus help docs explaining how access works.

If I were trying to buy gift cards today, these are the names I’d expect to run into first:

- Klarna: Built-in gift card shopping plus pay-later and financing options.

- Afterpay: App-based e-gift cards with the first payment taken at checkout.

- Zip: Gift cards in the app, split into four installments over six weeks.

- Sezzle: A buy now, pay later platform with a dedicated gift-card page, though gift card access is tied to Premium or Anywhere.

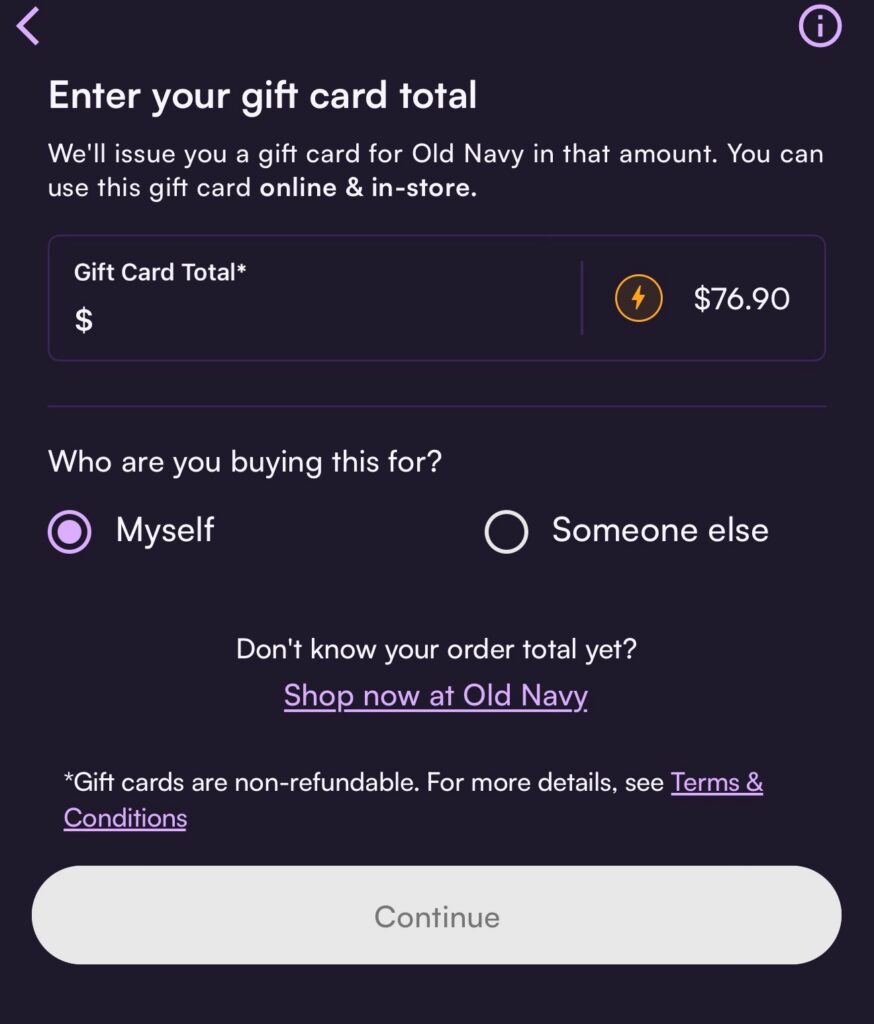

What It Looks Like Inside the Sezzle App

This is one area where Sezzle stands out to me, because it doesn’t just allow gift cards—it actually builds the experience around them.

Inside the app, there’s a full gift card section that feels more like browsing a mini marketplace than checking out at a single store. You can scroll through different categories, search brands, and even see deals or rewards attached to certain cards. It’s not buried or hard to find—it’s clearly designed to be used.

When I used it, what stood out most was how flexible it felt. Instead of being locked into whatever a retailer offers at checkout, you can choose the exact store you want first and then decide how you want to pay.

The process itself is simple. You pick the brand, enter the amount, and then split it into payments. It follows the same straightforward pay-in-4 structure, which I personally prefer over anything that starts turning into long-term financing.

Where the Cards Usually Come From

A lot of this runs through gift-card marketplaces rather than directly through the brand you’re gifting. Giftcards.com is one of the bigger examples right now, with hundreds of brands plus digital and physical options. It also sells a Visa card, which is useful if you want something more flexible than a single-store gift.

That’s also why you’ll see language about top brands and digital delivery all over these checkout pages. In practice, you’re often picking from a marketplace catalog, not buying straight from one retailer’s own checkout flow.

Digital Usually Makes More Sense

For this category, e-gift cards are usually the cleaner option.

If I’m sending gift cards, I usually go with digital delivery because that’s the easiest part of the whole thing. You can send them by email or text, and you don’t have to deal with shipping costs. Unless you specifically want a physical card, paying extra just to mail a gift card can feel a little unnecessary.

What I’d Check Before I Click Anything

This is the part I wouldn’t rush.

- How the split actually works: I always want to see how the payments are broken up. A small monthly payment can look fine at first, but there’s a big difference between a simple pay-in-4 plan and something that stretches out much longer.

- Whether financing changes the cost: Klarna’s longer-term financing disclosures show that plans can carry an annual percentage rate as high as 35.99%, and those offers are still subject to credit approval.

- Refunds and cancellations: Afterpay’s help page says gift cards bought through its system are non-refundable and can’t be canceled, which is a pretty big thing to know before checkout.

- Fees and fine print: This is where I watch for hidden fees and late fees. Afterpay says late fees may apply to gift card purchases, and Klarna’s one-time card disclosures mention a service fee for some bi-weekly payments.

I also care a lot more about the total purchase than the first payment. That’s especially true if the total purchase amount starts creeping up because you’re grabbing several cards at once and telling yourself future-you will deal with it.

When This Actually Makes Sense

I think this makes the most sense when you’re covering a big purchase in gift-card form, like holiday gifting for multiple people, employee rewards, or one flexible card for someone whose tastes you do not feel like guessing.

Where I’d be more careful is using BNPL just because it feels clever for your next purchase. Gift cards already turn cash into store-specific spending, so financing them only makes sense if the timing genuinely helps and the math still looks normal when you step back from it.

Final Verdict

Gift cards are easy. The payment side usually isn’t.

Splitting up the cost of a gift card can be helpful, especially when you’re buying several at once. I’d just want to make sure the payment setup makes sense and that I’m not making a basic purchase more complicated than it needs to be.

Personally, Sezzle is my favorite way to grab gift cards and pay over time. Learn more here.

FAQs

Yes, in some cases. A few major BNPL providers allow gift card purchases, but the rules vary quite a bit from one platform to the next.

Sometimes, but not always. Shorter pay-in-4 plans are often interest-free, while longer financing options may charge interest depending on the provider.

Usually not. Gift cards often come with stricter refund and cancellation rules, so it’s smart to check those before you buy.

Sometimes. Some providers let you use a virtual card, but merchant restrictions can still apply, so it’s not guaranteed to work everywhere.

Look at the payment structure, any fees, the return policy, and whether the gift card can actually be used the way you expect.