Apps like Klarna, typically your standard Pay-in-4 buy now, pay later apps, have more than 365 million users across the globe—and that number is only expected to grow.

That said, an app that’s popular may not always be the best fit for you.

Here are some of the top Klarna alternatives, alongside best-fit user recommendations, pros, and features to watch out for.

Key Takeaways

- Choose Sezzle if you want BNPL to feel simple, organized, and easy to use in real life, with flexible short-term plans, a virtual card, optional credit building, and rewards.

- Choose PayPal Pay Later if you already use PayPal everywhere and want the easiest possible online checkout.

- Choose Affirm if you are financing something larger and want more structured monthly plans.

- Choose Zip if your priority is reach and wallet-based flexibility online or in-store.

- Choose Afterpay if you want a classic pay-in-4 app with strong retail coverage and in-store wallet support.

Sezzle: Effortless Day-to-Day Use

Sezzle is the first Klarna alternative I’d look at because it’s so seamlessly blended into my day-to-day life. The short-term plans are clear, the app is easy to follow, and it does not feel like it is trying to turn every purchase into a mini loan.

Officially, Sezzle supports Pay in Full, Pay in 2, Pay in 4, Pay in 5, and long-term financing options on eligible purchases, so it is more flexible than people sometimes assume at first glance.

What really sets Sezzle apart is how much useful functionality it packs into the app. Sezzle Anywhere is a subscription-based feature that unlocks a multi-use virtual card, and Sezzle says it can be used anywhere Visa is accepted in the U.S., with availability and pricing varying by shopper. That makes it feel more like a real, everyday payment tool rather than something that only works when a retailer happens to show a BNPL button at checkout.

It also has extras that actually make sense. Sezzle Up lets you opt in to credit reporting, and Sezzle Spend gives you reward credits that Sezzle says can come from promotions and some Pay-in-Full purchases.

On the fee side, Sezzle doesn’t pretend every transaction is automatically free; it does say fees are reflected at checkout when they apply, which is exactly how a payment app should handle that.

- Best Fit: Someone who wants BNPL to feel like a budgeting tool, not a shopping rabbit hole.

- Pros: Simple short-term plans, a very usable app, strong virtual-card flexibility, optional credit building, and occasional rewards and credits.

- Watch For: Some features are subscription-based, and fees can apply depending on the order or Sezzle product you use.

PayPal Pay Later: PayPal Integration for Online Shopping

PayPal Pay Later is the most obvious alternative if you already use PayPal regularly and don’t want to learn a whole new ecosystem. PayPal offers Pay in 4 and Pay Monthly for qualifying purchases, with Pay in 4 splitting the cost into four payments every two weeks. PayPal also says Pay in 4 is available for eligible cart values between $30 and $1,500 when you check out with PayPal.

The main reason to pick PayPal is convenience. It works with millions of online merchants that accept PayPal, and it keeps everything within a payment flow many shoppers already trust. If your ideal BNPL option is “the one that adds the least friction,” PayPal has a strong case.

- Best Fit: Someone who mostly shops online and wants a pay-later option without downloading a more shopping-driven BNPL app.

- Pros: Familiar checkout, strong online acceptance, simple Pay in 4 option, and longer monthly financing available.

- Watch For: It is more useful as an online checkout tool than as a broad in-store or app-led BNPL system.

Affirm: For Bigger Purchases

Affirm is the alternative I’d look at for bigger purchases. It still offers Pay in 4, but its identity is much more tied to longer monthly plans. Shoppers may see 3-, 6-, or 12-month plans, and longer, and users see any interest up front before agreeing. There are also no fees charged.

That makes Affirm feel more like structured financing than lightweight checkout splitting. If you are buying furniture, travel, electronics, or anything else where lower monthly payments matter more than a quick six-week payoff, Affirm is often the cleaner comparison. The Affirm Card takes that even further by letting users request to pay over time in the app and then swipe to complete the purchase.

- Best Fit: Someone financing a larger purchase who wants fixed monthly terms and a very clear total before committing.

- Pros: Stronger, longer-term options, no fees, transparent plan setup, and card-based flexibility.

- Watch For: Some plans do include interest, so that it can feel more like a real loan product than a casual pay-in-4 app.

Zip: Plenty of Merchant Partners

Zip is the app I’d look at if your biggest issue with Klarna is merchant reach. With Zip, you can split nearly any purchase into four installments over six weeks, and it relies heavily on using a virtual card in the app. It also supports Apple Pay and Google Pay, which makes its in-store story more compelling than many checkout-only BNPL options.

That is the key difference with Zip: it feels like an access-first BNPL app. You open the app, create the virtual card, and take it with you. If you shop across a lot of different merchants and care more about “will this work here?” than “does this app have rewards or credit-building features?” Zip makes a lot of sense.

- Best Fit: Someone who wants a BNPL app that can move around with them instead of depending on a retailer’s native checkout button.

- Pros: Strong merchant reach, in-store wallet use, app-first virtual-card model.

- Watch For: It is more app-dependent, and the experience is less about perks or long-term tools than simple reach and flexibility.

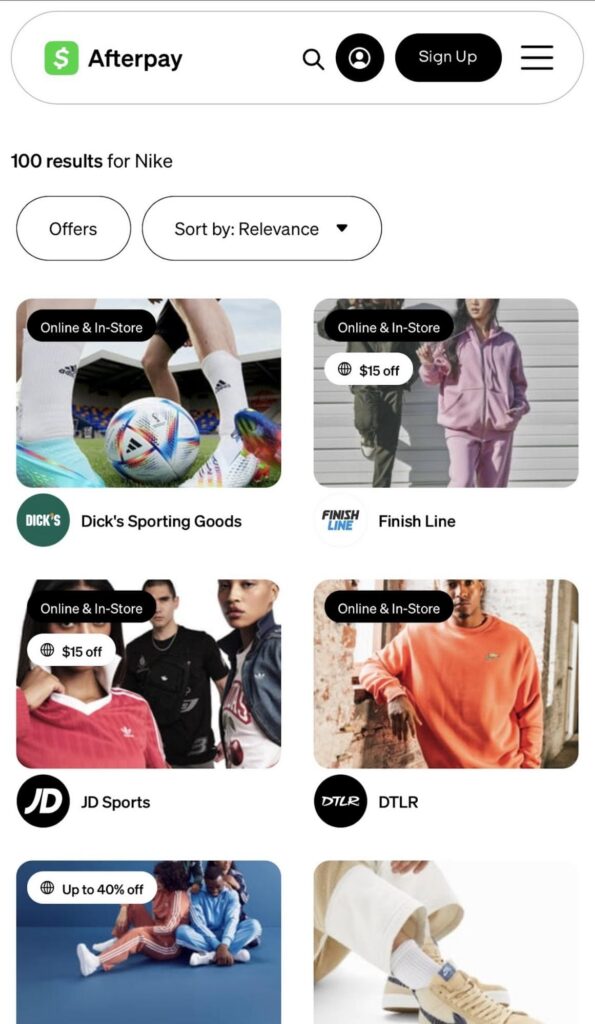

Afterpay: Retail-First Shopping

Afterpay is still one of the easiest Klarna alternatives to understand. The core appeal is straightforward: pay in 4, online or in-store, at many recognizable brands. Afterpay says shoppers can use it at thousands of brands and millions of products, and its in-store setup works through a digital Afterpay Card added to Apple Wallet or Google Wallet.

It has also become a little broader than its old “just pay in 4” reputation. Shoppers can choose 3-, 6-, 12-, or 24-month plans at partner brands, in addition to the standard four-payment option. So it still feels retail-first, but not quite as narrow as it used to be.

I personally love that you can search for a brand like Nike and it will show you all of the places you can use Afterpay to shop for it, and even offers discounts.

- Best Fit: Someone who wants a very familiar pay-in-4 retail app and shops often with mainstream brands.

- Pros: Recognizable checkout flow, strong retail coverage, easy in-store wallet use, and some longer-term options at partner brands.

- Watch For: Afterpay still feels most natural for retail shopping, not as a general-purpose financial tool.

A Few More Global BNPL Names Worth Knowing

If you’re outside the U.S. (or if you’re just curious, like I am), a few other names are worth knowing, too.

- Tabby: One of the biggest BNPL brands in the Gulf region, especially in Saudi Arabia, the UAE, and Kuwait. It also offers a Tabby Card for broader spending flexibility.

- Tamara: Another major player in the GCC, with installment options and a strong presence across Saudi Arabia and nearby markets.

- Zilch: A well-known UK option that supports both online and in-store use, with a virtual card and a mix of pay-now and pay-later features.

- Scalapay: A strong BNPL name in Southern Europe, especially in markets like Italy, Spain, and France.

- Atome: A major BNPL app across Southeast Asia, with broad use in categories like fashion, beauty, travel, and home.

Bottom Line

Here are the basics: Sezzle is a good place to start because it offers simple short-term plans and useful app features. PayPal, Zip, Affirm, and Afterpay can also work well, depending on your needs. Your experience will vary based on where you shop, how long you want to pay things off, and how much flexibility you need from the app. In the end, the best way to find out which one suits you is to try them yourself.

FAQs

What are the most popular apps like Klarna?

Some of the biggest Klarna alternatives include Sezzle, PayPal Pay Later, Affirm, Zip, and Afterpay. They all let you split purchases over time, but they differ quite a bit in flexibility, plan types, and how they fit into everyday shopping.

Which BNPL app is best for simple short-term payments?

If you want something that feels easy to use and straightforward to manage, Sezzle is one of the better options to look at. It keeps the focus on short-term payment plans and app-based flexibility instead of turning the whole experience into a shopping feed.

Are apps like Klarna all basically the same?

Not really. Some are better for longer monthly financing, some work better in-store, and some feel more useful for everyday online shopping. The structure may look similar at first, but the experience can feel pretty different once you actually use the providers.

Which Klarna alternative works best for larger purchases?

Affirm is usually the one people look at for larger purchases because it offers longer monthly plans. That said, it tends to feel more like structured financing than a simple pay-in-4 app, so it really depends on what kind of purchase you’re making.

Can you use BNPL in real stores?

Sometimes, yes. Some providers offer virtual cards or wallet-based options that enable in-store use, while others are more tied to online checkout. That’s one of the bigger differences to compare before choosing one.