50% of young consumers prefer buy now, pay later over credit cards, and it’s easy to see why—you’re basically carrying over balances without having to pay the APR.

But when comparing BNPL providers, like Sezzle vs. Afterpay?

Making the right choice can feel difficult.

The good news is, I’ve used both myself. While both have their use cases and can ease your financial stress, I have a strong preference. Let’s break it down.

Key Takeaways

- If you want more control over your payments, go with Sezzle: Sezzle is the better fit if you care about payment visibility, rescheduling options, and a more budgeting-focused app experience.

- If you want a smoother, more shopping-friendly app, go with Afterpay: Afterpay feels more polished on the retail side and works well for quick purchases at popular stores.

- If you want BNPL to support better financial habits, go with Sezzle: Sezzle Up gives users optional credit reporting, which makes it more useful for shoppers who pay on time and want that to count for something.

- If you know you won’t need much flexibility once the plan starts, go with Afterpay: It works well for shoppers who just want a straightforward pay-in-4 setup and expect to stay on schedule without needing adjustments.

- If you want a virtual card that feels more useful day to day, go with Sezzle: Sezzle Anywhere adds broader spending flexibility, which makes the app feel more practical beyond basic checkout buttons.

Sezzle: Short-Term Flexibility With More Payment Control

Sezzle works best when I want BNPL to feel like a budgeting tool instead of a shopping toy. The core product is still short-term installment splitting, but Sezzle now offers more variety than people sometimes realize: Pay in 2, Pay in 4, Pay in 5, Pay in Full, and monthly installment plans on eligible purchases. It may run a soft credit check to determine spending power, but Sezzle says standard use does not negatively impact your credit score.

What keeps me coming back is that Sezzle gives me more room to adjust when real life gets messy. Qualifying orders can be rescheduled, sometimes more than once, and Premium or Anywhere subscribers get one extra free reschedule per order. Sezzle Up also lets shoppers opt in to credit reporting, which is still unusual in BNPL.

And Sezzle Anywhere gives you a subscription-based multi-use virtual card that can work online or in-store wherever Visa is accepted in the U.S., with some exceptions. I love my Anywhere subscription because of all of the perks I get.

Pros

✅ Clear short-term plan options, including Pay in 2, 4, and 5

✅ Self-service rescheduling on qualifying orders

✅ Optional credit reporting through Sezzle Up

✅ Strong app utility, especially with Sezzle Anywhere and the virtual card

Cons

❌ Service fees can apply, especially on some virtual-card or merchant setups

❌ The most flexible version of Sezzle is not always the free version

❌ Monthly plans can carry interest depending on the offer and credit profile

Afterpay: Smoother Retail Shopping, Less Forgiving

Afterpay feels more retail-first to me. The app is polished, the checkout flow is slick, and it is very clearly built around shopping. Its standard setup is still Pay in 4 over six weeks, with the first payment due at checkout, but it now also offers Pay Monthly plans of 3, 6, 12, or 24 months on eligible purchases over $100. For standard onboarding, Afterpay says it may conduct a soft credit check for new customers, and that soft pull does not affect your credit score.

I get why people like it. I was approved for decent buying power quickly, and when I used it to purchase a concert ticket, the plan itself was easy to understand. But Afterpay feels less forgiving once you’re in motion. Your spending limit is tailored to your history, and Afterpay says new users may be limited to fewer purchases at first.

It also says orders can be declined for several reasons, even if you have used the service before, and that if you need help moving a payment date, the available help is narrower and more conditional than Sezzle’s self-serve reschedule flow.

Pros

✅ Very polished app and checkout flow

✅ Strong retail coverage online and in-store

✅ Straightforward Pay in 4 structure

✅ Pay Monthly gives more time for bigger purchases

Cons

❌ Less self-service flexibility once a payment plan starts

❌ Spend limits and approvals can feel a little opaque

❌ It is easier for the app to feel like a shopping mall than a budgeting tool

Sezzle vs Afterpay Side-By-Side Comparison

| Feature | Sezzle | Afterpay |

|---|---|---|

| Standard short-term plan | Pay in 2 / 4 / 5 on eligible purchases | Pay in 4 |

| First payment timing | At checkout | At checkout |

| Credit check | Soft check may be used for spending power | Soft check for new customers; no score impact |

| Credit reporting | Optional through Sezzle Up; reports payment history to credit bureaus if you enroll | Says it does not currently report to U.S. credit bureaus |

| Rescheduling | Available on qualifying orders; fees may apply; extra free reschedule with Premium/Anywhere | More limited payment-date help; some payments cannot be changed |

| In-store use | Multi-use virtual card through Sezzle Anywhere via Apple Pay / Google Pay | Afterpay Card via Apple Wallet / Google Wallet if eligible |

| Fees | Service fees may apply; reschedule fees may apply; monthly plans may carry interest | No late fees when paid on time; late fees may apply after the grace period; finance fees can apply on some single-use or gift-card Pay in 4 purchases; monthly plans may carry APR |

| Longer financing | Monthly installment plans from 3 to 36 months on eligible purchases | Pay Monthly plans from 3 to 24 months on eligible purchases |

Payment Flexibility And Real-Life Budgeting

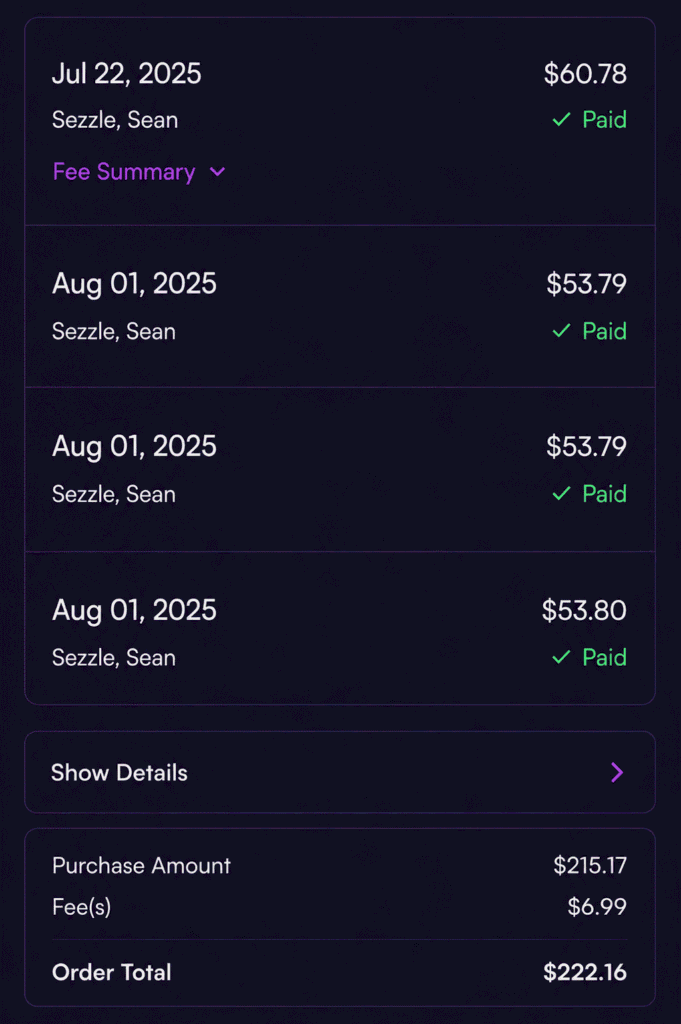

On paper, both let you split a purchase into four interest-free payments over six weeks. In actual use, though, Sezzle gave me a lot more breathing room. I used it during a tight back-to-school week on a $216 purchase and paid a little over $60 upfront, including a small service fee. What made the difference was not just the lower upfront hit. It was being able to reschedule a payment once for free when timing got tight.

That kind of flexibility matters more than people admit. A paycheck comes in late. A utility bill lands in the same week as rent. A travel cost shows up at the worst possible time. Sezzle felt built for that kind of real-life budgeting messiness.

Afterpay felt more rigid. I used it for a $380 concert ticket purchase, and the original setup was easy enough. It split the cost into four automatic payments, and the app looked polished while doing it. But the moment I started thinking past the original purchase, it felt less forgiving. One missed payment or timing issue seems to create more friction, and there is not the same built-in room to adjust.

Winner: Sezzle. Both apps split purchases into four payments, but Sezzle gives users more room to manage real-life timing problems without everything feeling so fragile.

Credit Building And Long-Term Value

If I am using BNPL responsibly, I want that to count for something. Sezzle gives users the option through Sezzle Up, which can report payment history to all three major credit bureaus. That makes the app feel like more than just a way to delay a purchase. It can actually support better financial habits over time.

That matters even more now that BNPL activity is expected to matter more in credit scoring going forward. If I am paying on time and staying on top of my schedule, I would much rather use the app that gives me some upside for doing that.

Afterpay does not really offer the same thing. Paying on time does not do much for you long term, but if things go badly enough, you can still end up dealing with the downside. That imbalance bothers me. It makes Afterpay feel more transactional, while Sezzle feels a little more useful beyond the immediate checkout moment.

Winner: Sezzle. Sezzle gives on-time users a clearer long-term benefit, which makes it a better fit for shoppers who want BNPL to support stronger financial habits.

Fees, Penalties, And What The Cost Really Looks Like

With Sezzle, I do not think the fee structure is perfect, but I do think it is easier to work with. On that $216 purchase, I paid a small service fee upfront, so I knew exactly what I was dealing with. Sezzle can also charge a $1.50 fee if you use a debit card instead of a linked bank account, and extra reschedules can cost somewhere around $5 to $7.50, depending on the situation. So no, it is not magically fee-free. But the structure still feels more transparent and easier to plan around.

Afterpay skips the upfront service fee, which sounds better at first. But the tradeoff is that missed payments can trigger late fees of up to $8, and the bigger issue for me is what happens around spending power. If something goes wrong, the app can get a lot stricter very quickly.

I was declined on a later purchase even though my earlier orders had been paid on time, and I have seen other users describe sudden limit drops that took forever to recover from. One example that stuck with me was a user whose limit dropped to $50 after paying off a $30 balance, and it took more than a year and a half to come back.

So even if Afterpay looks cleaner on the fee side at first glance, I do not think it always feels lighter once you factor in how quickly the app can tighten up.

Winner: Sezzle. Sezzle’s fees are not my favorite, but they still feel more predictable and easier to work around than Afterpay’s stricter penalty-and-limit dynamic.

App Experience And Day-To-Day Use

Afterpay looks better. The app is smoother, more polished, and more shopping-friendly right away. When I used it for that $380 concert ticket purchase, the visual flow felt clean and easy to follow. It is clearly built to make shopping feel simple, and in that sense, it does its job really well.

Sezzle is better for me once the shopping part is over. I like the dashboard more because it works better as a money tool. I can quickly see what is due today, what is coming next, how much spending power I have, and where to go if I need to manage a payment. I also liked that Sezzle’s virtual card worked smoothly with Apple Wallet, while Afterpay’s one-time virtual card felt slower and clunkier during a time-sensitive Ticketmaster purchase.

So this really comes down to what kind of app experience you care about more. If you mean polish, browsing, and checkout flow, Afterpay wins. If you mean payment management after the purchase, I think Sezzle is better.

Winner: Afterpay. Sezzle works better as a payment-management tool, but Afterpay has the smoother, more polished shopping app overall.

Final Verdict

After using both, I think Sezzle is the better BNPL option for people who want more control over their payments, more visibility inside the app, and more room to deal with real-world budget timing. It is not the cheapest possible option in every scenario, and some of the best extras are tied to subscription products, but the overall experience feels more thoughtful and more useful once life gets even a little messy.

Afterpay is still a good app. I get why people use it. It’s polished, easy to shop with, and perfectly workable for quick interest-free retail purchases. But if I am picking one for actual budgeting, day-to-day payment management, and long-term financial habits, Sezzle edges it out. It feels less like an app that wants me to keep shopping and more like one that actually helps me stay in control.

FAQs

Is Sezzle or Afterpay better for budgeting?

Sezzle is usually the better fit for budgeting because it gives users more visibility into what is due, what is coming next, and where to adjust payments if needed. It feels more like a payment-management tool than a shopping app.

Do Sezzle or Afterpay help build credit?

Sezzle can, if you enroll in Sezzle Up. Afterpay does not currently give the same kind of positive credit-building benefit for standard on-time payments.

Which app is easier to use in everyday life?

That depends on what you mean by “easier.” Afterpay feels smoother on the shopping side, but Sezzle tends to feel more useful once you care about tracking payments, managing timing, and staying organized.

Are Sezzle and Afterpay both interest-free?

Both can be interest-free on standard short-term plans when payments are made on time. The bigger differences usually show up in fees, flexibility, and whether longer-term options are involved.

Who should choose Afterpay instead of Sezzle?

Afterpay makes more sense for shoppers who want a very simple retail BNPL experience and do not expect to need much payment flexibility later. If you are confident the standard schedule will work for you, it can still be a solid option.