The average household spends $10,000 on food every single year.

Buy now, pay later food aims to make that $10,000 sting a little less by spreading the amount over time.

But how do you use it? Where can you use it? And most importantly, should you use it?

As a BNPL user myself, I’ve put in the research and experience to answer it all for you. Let’s get started.

Key Takeaways

- BNPL Can Smooth Cash Flow: It helps split food costs into smaller payments, so one grocery trip does not drain your account all at once.

- Pay In 4 Is Often The Sweet Spot: It is usually interest-free, simple to track, and best for everyday grocery or food delivery purchases.

- Longer Plans Can Still Make Sense: Paying some interest may be worth it when smaller payments give your budget more breathing room.

- Always Check The Total Cost: Look beyond the monthly payment and make sure the final amount still feels worth it.

- Use BNPL With A Plan: It works best for groceries, pantry restocks, meal kits, and planned food purchases you already know you can repay.

What Is Buy Now, Pay Later Food?

Buy Now, Pay Later food means using a BNPL service to pay for food-related purchases over time.

That may include groceries, restaurant orders, food delivery, meal kits, warehouse club runs, specialty food, coffee, snacks, or bulk pantry items. Some BNPL options are built into checkout. Others work through an app, digital card, or one-time virtual card.

The main idea is simple: you get the food now, then pay in smaller pieces.

That can be useful when your grocery trip is bigger than normal, payday is a few days away, or you want to keep more money in your account for bills, gas, rent, or other needs.

BNPL Food Providers

So, where can you actually use buy now, pay later services for food?

The list is actually pretty extensive.

- Food Delivery Services: GrubHub, Uber Eats, DoorDash, Instacart

- Pizza Places: Domino’s, Pizza Hut, Papa John’s, California Pizza Kitchen

- Casual Dining: Texas Roadhouse, Outback Steakhouse, Red Lobster, Chili’s, Applebee’s

- Cafes: Starbucks, Krispy Kreme, Dutch Bros, The Coffee Bean and Tea Leaf

- Fast Food: Taco Bell, Chipotle, Jersey Mike’s, Five Guys, Steak N’ Shake,

- Grocery Stores: Walgreens, Costco, Walmart, Target, Kroger

Sezzle partners with all of these providers and more, so they’re my #1 pick for food BNPL.

How BNPL Works for Food Purchases

BNPL usually works in a few steps.

You shop like normal. At checkout, you choose a BNPL option if it is offered. You may need to log in, apply, or get a quick approval. Then you pick a payment plan, review the cost, and confirm the purchase.

The most common option is Pay in 4. With Pay in 4, your total is split into four payments. You usually pay the first part right away, then the rest every two weeks.

So, if your grocery order is $120, a Pay in 4 plan may look like this:

| Food Purchase | Payment Style | What You Might Pay | Best For |

|---|---|---|---|

| $80 grocery order | Pay in 4 | $20 today, then $20 every two weeks | Smaller weekly grocery trips |

| $160 warehouse club run | Pay in 4 | $40 today, then $40 every two weeks | Bulk food, pantry restocks, family shops |

| $300 meal kit or food stock-up | Monthly plan | Smaller monthly payments, possibly with interest | Bigger orders where cash flow matters more |

| $45 takeout order | Pay in 4, if available | Around $11.25 per payment | Treat meals without one full hit today |

Pay in 4 is often the cleanest choice because it is usually interest-free. The tradeoff is that the payments come faster, and each payment may be higher than a longer monthly plan.

That is why the “best” plan depends on your real life. If four quick payments fit your budget, great. If a longer plan gives you more breathing room, that can be worth considering too.

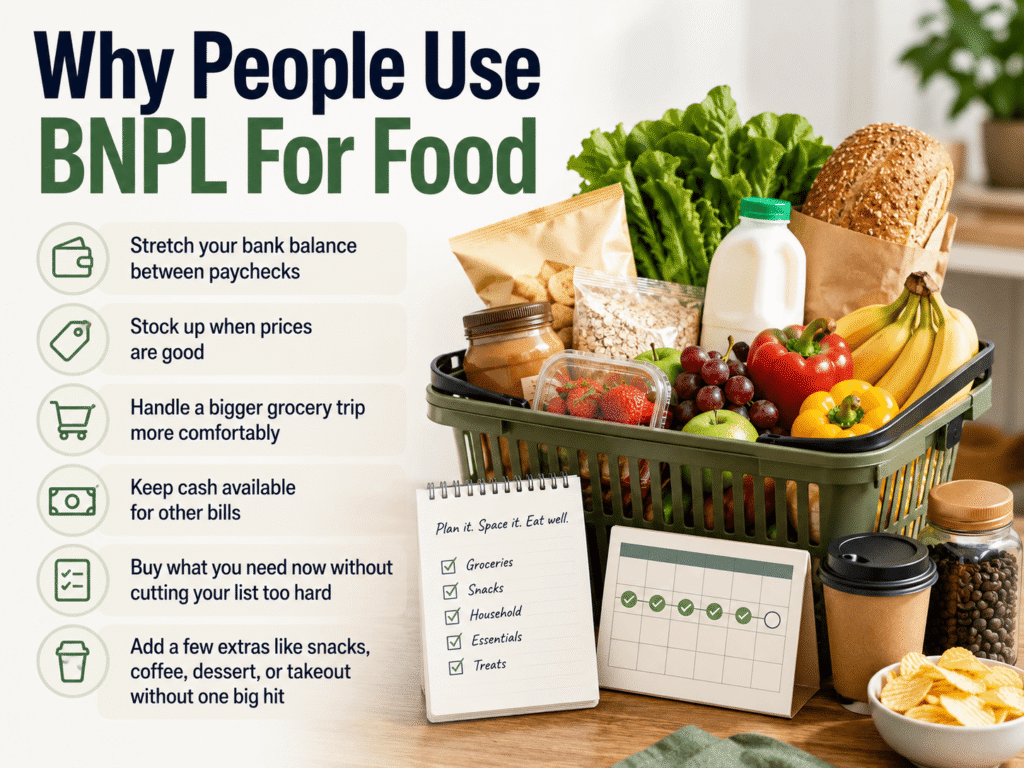

Why People Use BNPL for Food

People do not use BNPL for food because they are confused about money. They use it because food costs are real, timing matters, and cash flow can be tight even when you are doing fine overall.

A $180 grocery order may be totally reasonable. But paying it all today can still feel annoying if your phone bill, gas, and rent are also pulling from the same account. BNPL can smooth that out.

It can help you:

- Stretch your bank balance longer between paychecks.

- Stock up when prices are good.

- Handle a larger grocery trip without draining your account.

- Keep cash available for other bills.

- Buy what you need now instead of cutting a grocery list too hard.

- Add a few wants, like snacks, coffee, dessert, or a takeout night, without one big hit.

This is where BNPL can feel genuinely useful. It is not just about buying more. It is about timing.

A lot of personal finance advice acts like every purchase should be judged only by the total price. But timing matters too. Paying $150 all at once can feel very different from paying $37.50 four times, even if the total is the same.

Top Tips for Using BNPL for Food

Here is the practical part. BNPL works best when you treat it like a cash flow tool, not free money.

- Use Pay in 4 when the payments fit. It is often interest-free and easy to understand.

- Choose a longer plan only when the lower payment is worth the extra cost. Interest is not always a dealbreaker, but it should be clear.

- Check the total before you hit confirm. The monthly payment matters, but the full repayment amount matters more.

- Match payments to paydays. If possible, pick a plan that lines up with when money lands in your account.

- Use it for real food plans. Groceries, pantry restocks, meal kits, and planned takeout are better fits than random impulse orders.

- Keep one eye on your open plans. A few small food payments can add up if they all hit in the same week.

- Save BNPL for moments where it actually helps. It is most useful when it smooths your budget, not when it creates clutter.

That is really the whole game: use BNPL to make your money feel less squeezed, while still staying clear on what you owe.

Bottom Line

BNPL for food makes sense when it helps you manage timing. If you know the payments fit, it can make groceries, delivery, meal kits, or bulk food orders easier to handle. It can help your bank account last longer and keep your cash flow steady.

Used responsibly, Buy Now, Pay Later food is not some scary thing. It is a flexible payment tool. For many people, that flexibility matters.

FAQs

Can you use Buy Now, Pay Later for groceries?

Yes, some grocery stores, delivery apps, and BNPL providers allow food purchases. Availability depends on the store, app, and payment method.

Is Pay in 4 good for food purchases?

Pay in 4 can be a strong choice because it usually splits the cost into four interest-free payments. It works best when the payment schedule lines up with your budget.

Can you use BNPL for takeout or food delivery?

In some cases, yes. Certain delivery platforms, restaurants, or BNPL apps may allow it, especially through app checkout or a virtual card.

Is it bad to pay interest on BNPL food purchases?

Not always. If the total cost is clear and the smaller payments help your cash flow, a longer plan with interest may still be useful.

What should you check before using BNPL for food?

Check the payment dates, total cost, fees, and whether the payments fit your upcoming budget. The goal is to make food spending easier, not harder.