There are plenty of apps like Zip out there: buy now, pay later (BNPL) providers that let you split the cost of purchases over time right on your phone.

But with 50+, if not hundreds, to choose from, finding the perfect fit can be tricky.

Don’t worry; I’ve done the research for you. And in this quick guide, I’ve outlined Zip’s top BNPL competitors alongside what makes them stand out.

Let’s get started.

Key Takeaways

- The Right BNPL App Depends On Your Shopping Style: Some apps are better for quick short-term splits, while others make more sense for larger purchases or broader checkout flexibility.

- Payment Structure Matters More Than Brand Name: The most important difference is usually how the plan works — whether you want pay-in-4, more time before the first payment, or a longer monthly option.

- Checkout Reach Can Change The Experience: Some BNPL tools work mainly at partner stores, while others offer virtual cards or broader in-store and online flexibility.

- Not Every App Is Built For The Same Kind Of User: Some feel more like budgeting tools, while others are clearly designed to make shopping feel smoother and more tempting.

- The Best Alternative Is Usually The One That Fits Real Life: The most useful BNPL app is the one that matches your budget, the places you shop, and how much payment flexibility you actually need.

Sezzle

Sezzle is the first one I’d look at if you like the idea of Zip but want something that feels more organized and easier to live with. It still covers the short-term installment side of BNPL, but it gives users more ways to structure a purchase and to manage what happens after checkout.

That is the part I like most. A lot of BNPL apps are decent at getting you through checkout. Fewer are good once real life starts happening around the payment schedule.

Sezzle has short-term options like Pay in 2, Pay in 4, and Pay in 5, plus monthly plans on some purchases. It also has Sezzle Anywhere, which is a big deal if you want broader use beyond a normal partner checkout page. The virtual card makes it feel more practical for day-to-day shopping, rather than only being useful when a retailer already has the BNPL button built in.

It also has features that feel more useful than decorative. Sezzle Up gives users a credit-building angle if they want one, and Sezzle Spend adds occasional credits and reward-style perks that can make the app feel a little more generous without turning it into a shopping circus.

What makes Sezzle stand out

- More short-term plan variety than many BNPL apps

- A virtual card through Sezzle Anywhere

- Optional credit-building through Sezzle Up

- A cleaner, more payment-focused app experience

Best for

People who want BNPL to feel like a money tool, not just a way to make checkout easier.

PayPal Pay Later

PayPal is the easiest alternative to understand because most people already know exactly what it is. If you already use PayPal at checkout, adding Pay in 4 or Pay Monthly usually feels pretty natural.

That’s the appeal here. It is not exciting, but it is convenient. You are not really learning a whole new ecosystem. You are just layering installments into a payment system you may already trust.

It is especially useful for online shoppers who do not want to think too hard about BNPL. You check out, you see the option, and you decide whether splitting the purchase makes sense. That simplicity is part of the value.

Where it is a little less interesting is personality. It doesn’t feel like a broader payment-management app like Sezzle, and it isn’t as specialized for larger financing as Affirm. It is more like the safe middle option.

What makes PayPal different

- Extremely familiar online checkout flow

- Good fit for people who already use PayPal regularly

- Short-term and monthly options without a very app-heavy feel

Best for

Online shoppers who want the least friction possible and do not care about having a separate BNPL lifestyle app.

Affirm

Affirm makes the most sense when your purchases are getting bigger, and Zip starts to feel a little too small-scale. It still has short-term options, but the real reason people use Affirm is longer financing.

That changes the tone of the whole app. Affirm feels less like “split this little purchase” and more like “let’s actually structure this purchase in a way you can live with.” For furniture, travel, electronics, and more expensive items, that can be a much better fit than a six-week payoff.

This is also where it feels more honest to call it financing instead of just BNPL. That is not necessarily bad. It just means it is better for people who actually want a longer runway and are willing to think about total cost a little more seriously.

What makes Affirm different

- Better known for longer monthly plans

- Better fit for larger purchases

- Feels more like structured financing than a casual retail app

Best for

People buying something expensive enough that “just split it into four” no longer feels realistic.

Afterpay

Afterpay is probably the most familiar pure retail BNPL option in the group. It still feels very tied to the classic “buy the thing now, split it into four, move on” model.

That is part of why people like it. It is easy to understand, easy to spot at checkout, and very comfortable if most of your BNPL use is fashion, beauty, shoes, gifts, or mainstream online shopping. It also tends to feel more polished on the shopping side than some of the more payment-focused apps.

Compared with Zip, Afterpay feels a little less like a flexible payment tool you carry around and a little more like a retail installment option that happens to be available in many places. That is not a flaw. It just means the vibe is different.

What makes Afterpay different

- Very recognizable retail BNPL setup

- Good for quick, mainstream shopping purchases

- Polished, shopping-friendly app experience

Best for

People who mostly use BNPL for regular retail shopping in search of something familiar and simple.

Klarna

Klarna is one of the biggest names in this space because it offers shoppers more ways to pay than most of its competitors. That flexibility is real. If Zip feels a little too one-note, Klarna can feel like the opposite.

It is not just a pay-in-4 app. It is more of a shopping platform with built-in financing. That can be useful if you like having multiple payment styles in one place. It can also be a little much if you just want to split a purchase and get out.

That is the tradeoff with Klarna. It is broader, more feature-heavy, and more shopping-driven. Some people love that. Some people find it distracting.

What makes Klarna different

- More payment structures in one app

- More shopping features and retailer discovery

- More “shopping ecosystem” energy than most BNPL apps

Best for

Shoppers who want options and do not mind an app that feels more like a retail hub than a strict payment tool.

| App | Best For | Key Features | Main Tradeoff |

|---|---|---|---|

| Sezzle | Shoppers who want more payment control and short-term plan variety | Pay in 2, Pay in 4, Pay in 5, monthly plans on eligible purchases, Sezzle Anywhere virtual card, Sezzle Up credit reporting option | Some of the most flexible features are tied to paid add-ons, and service fees can apply to some orders. |

| PayPal Pay Later | People who already use PayPal often and want an easy online checkout option | Pay in 4 for eligible purchases from $30 to $1,500, Pay Monthly for larger purchases, very familiar checkout flow | Feels more like an online checkout layer than a broader BNPL app. |

| Affirm | Bigger purchases that need longer monthly payments | Pay in 4, monthly plans for 3, 6, 12 months and longer, Affirm Card, no fees | Can feel more like traditional financing than a lightweight pay-later app. |

| Afterpay | Mainstream retail shopping with a classic pay-in-4 setup | Pay in 4 over 6 weeks, in-store Afterpay Card, monthly plans at partner brands | More retail-first and less “use it almost anywhere” than Zip or Sezzle-style virtual card setups. |

| Klarna | Shoppers who want more payment choices and a more feature-heavy app | Pay in 4, Pay in 30, pay in full, financing over time, one-time card, shopping tools | More shopping-driven, which can feel busy if you just want a simple payment app. |

Which Zip alternative actually makes the most sense?

That really depends on what you liked about Zip in the first place.

If you liked the flexibility, Sezzle is the strongest place to start because it combines broader real-world usefulness with a more practical, payment-focused app experience. The others can still make sense depending on what you need — PayPal for easy online convenience, Affirm for larger purchases, Afterpay for a familiar retail setup, and Klarna for shoppers who want more payment options in one app.

FAQs

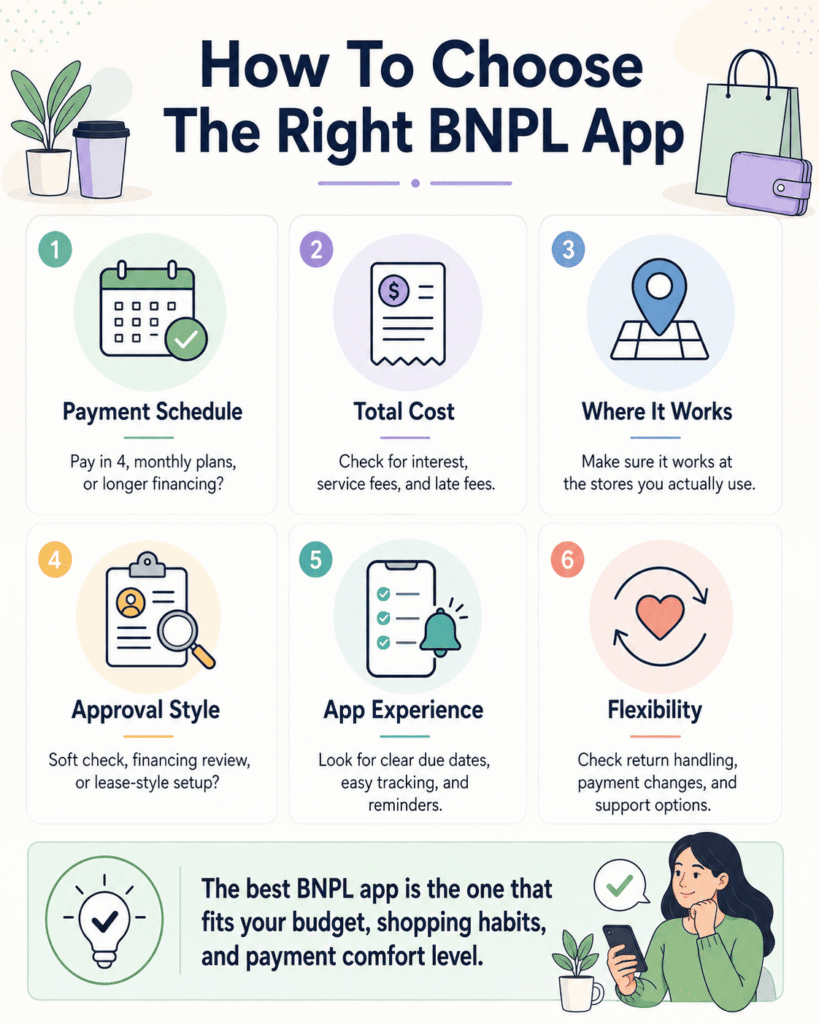

What should I look for when comparing apps like Zip?

Focus on how the payments work instead of the brand. The main things to compare are how much time you get to pay, where you can use the app, and whether it helps you budget or just makes shopping easier.

Are apps like Zip all basically the same?

No, they are not all the same. While they are all called BNPL apps, some work better for small, everyday buys, some are better for bigger purchases, and some can be used at more stores than others.

How do I know which BNPL app fits me best?

Consider your shopping habits. If you usually shop online, one app might suit you better. If you prefer shopping in stores, look for an app with a virtual card. If keeping track of payments is most important, pay attention to how easy the app is to use.

Is a broader payment network always better?

Not always. Having more places to use the app can be useful, but some people prefer a simpler app that makes it easier to manage payments, even if it works at fewer stores.

What matters more: flexibility or simplicity?

It depends on what you buy and how you like to shop. Some people want as many payment options as possible, while others prefer a simple plan that is easy to follow and keeps things predictable.