The average grocery spend for a single American adult is $350 a month and is quickly climbing.

That jumps to well over $1,000 for two adults with children in the mix.

It’s a lot to manage, but buy now, pay later groceries are rising in popularity: paying a sort of “down payment” to take them home, then spreading the rest of the cost over time.

But is BNPL groceries the right fit for you? And if so, how do you get started?

I’ve laid it all out for you below.

Key Takeaways

- Groceries Can Be Split Up: Buy now, pay later grocery options let you break a larger food bill into smaller payments instead of paying everything at once.

- Pay-In-4 Is The Common Setup: Most grocery BNPL plans use four payments, with the first due at checkout and the rest spread out over the next several weeks.

- Works at Many Retailers: BNPL can often be used with major grocery stores and delivery services, both online and sometimes in person through virtual cards.

- Not Every Purchase Qualifies: Standard grocery items usually qualify, but some plans may require a minimum purchase amount before you can use them.

- Terms Still Matter: Many short-term plans are interest-free, but longer installment options may include high APRs, so it’s worth checking the full cost first.

What Buy Now, Pay Later For Groceries Means

Buy now, pay later for groceries lets you split your food bill into smaller payments instead of paying everything at once. Usually, the BNPL company pays the store first, and you pay them back over time.

The main benefit for grocery shoppers is getting what they need now while keeping more money in their accounts. This can help if you’re juggling rent, gas, tuition, or other bills. Companies like Klarna, Zip, Sezzle, PayPal, and Affirm offer these short-term payment plans, but the details depend on the store and the app.

How Grocery BNPL Payments Usually Work

The most common setup is pay-in-4. You pay the first part at checkout, and the rest is charged automatically every two weeks, usually over six weeks in total.

This setup is popular because it’s usually interest-free, simple to understand, and helps with short-term budgeting. The downside is that the payments come quickly and can feel a bit large.

Some providers also have longer monthly plans. These can help if you want smaller payments and more time to pay. Just make sure to check the total cost, since longer plans might include interest.

Where You Can Use BNPL For Groceries Online And In Store

You can use BNPL for groceries in two main ways: right at checkout with stores that offer it, or by using a BNPL app that gives you a virtual card.

Big retailers and grocery services offer BNPL through partners; Sezzle is one of the most popular. Depending on the app, you might find BNPL at stores like Walmart, Amazon, Target, Costco, Whole Foods, Instacart, and HelloFresh.

In stores, using app-based virtual cards can give you more options. If the store takes the digital wallet or card linked to the app, you can use BNPL even if it’s not advertised.

| Option | How it usually works | Best for | Watch out for |

|---|---|---|---|

| Pay in 4 | Four payments over a short period, often interest-free | Travelers who can handle larger payments quickly | Payments come fast |

| Monthly plan | Smaller payments over a longer term, may include interest | Travelers who need more breathing room | Higher total cost |

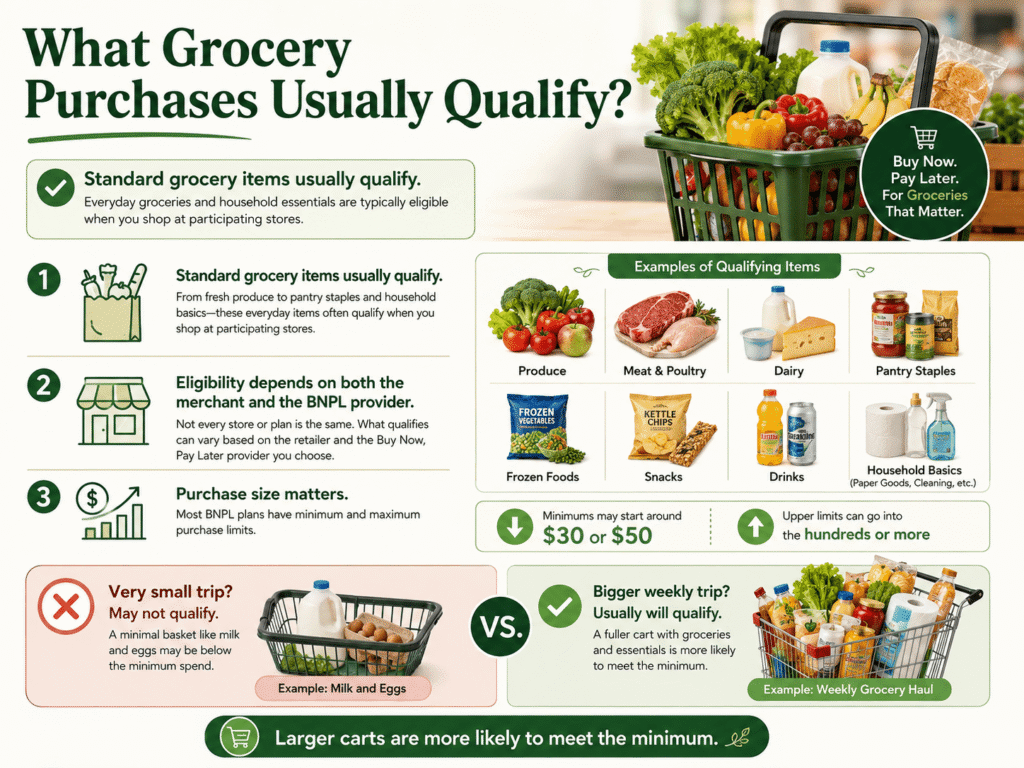

What Grocery Purchases Are Typically Eligible

Usually, standard grocery items qualify: produce, meat, dairy, pantry staples, frozen foods, snacks, and drinks. Eligibility depends on both the merchant and the BNPL provider.

The other big factor is purchase size. Many plans have minimum and maximum spending limits. For example, some providers start around $30 or $50, while upper limits can reach well into the hundreds or more.

So, a quick trip for just milk and eggs might not qualify, but a bigger weekly shopping trip usually will. If you add household items like paper goods or cleaning products, it’s easier to meet the minimum.

Fees, Credit Checks, And Credit Score Impact

Details are important here. Many pay-in-4 grocery plans don’t charge interest and only use a soft credit check, or sometimes none at all. This makes them appealing to people who want flexibility without using a high-interest credit card.

But not all plans are free. Longer payment options can have interest rates, sometimes high ones, so always check the total amount you’ll pay, not just the monthly payment.

If you pay late, you might get charged fees, lose access to BNPL, or even face collections. Credit reporting depends on the provider, so paying on time may not help your credit, but missing payments can still cause issues.

Before using BNPL for groceries, check:

- Whether the plan is interest-free

- Whether there’s a soft credit check

- Whether late fees apply

- Whether missed payments can affect your credit

- Whether there’s a minimum or maximum purchase amount

When Using BNPL For Groceries Makes Sense

BNPL works best for short-term timing issues, not long-term money problems. If your paycheck is coming soon, but isn’t here just yet, splitting up your grocery bill can be a helpful solution.

It can also help you keep cash available for other bills that are due now, like rent, utilities, or exam fees. This flexibility can be really useful.

The best way to use BNPL is with a no-interest pay-in-4 plan for a bigger grocery trip that you know you can pay off in the next month. If you need more time, a longer plan can help, but make sure the interest is worth the convenience and reduced stress.

Bottom Line

Buy now, pay later for groceries can be useful when the issue is timing, not affordability. If you need to cover a larger grocery trip before your next paycheck hits, splitting the cost can give you a little breathing room without throwing off the rest of your budget.

It works best when the plan is interest-free, the payments are manageable, and you already know you can pay it off quickly. Used that way, it can be a practical short-term tool instead of a longer-term problem.

FAQs

What does buy now, pay later for groceries mean?

Buy now, pay later for groceries lets you split your grocery purchase into smaller installments instead of paying the full amount at checkout. A BNPL provider pays the store upfront, and you repay them over time, usually with no interest if paid on schedule.

How do buy now pay later grocery payments usually work?

Most grocery BNPL plans split payments into four installments over about six weeks. You pay the first installment at checkout, then the rest is auto-charged every two weeks. These plans are often interest-free and help manage short-term budget pressure.

Where can I use buy now, pay later options for groceries?

You can use BNPL for groceries online and in-store at major retailers like Walmart, Amazon, Target, Costco, Whole Foods, Instacart, and HelloFresh. BNPL apps also offer virtual cards that work wherever their digital wallets are accepted.

What types of grocery items typically qualify for buy now, pay later payments?

Standard grocery items such as produce, meat, dairy, pantry staples, snacks, and drinks usually qualify. Eligibility depends on the merchant and BNPL provider, with minimum purchase amounts generally starting around $30 or $50.

Does using buy now, pay later for groceries affect my credit score?

Many BNPL plans use soft credit checks or none at all, so on-time payments usually don’t impact credit scores. However, missed or late payments can lead to fees, collections, and possibly hurt your credit if reported to bureaus by the provider.

When is it a good idea to use buy now, pay later for groceries?

BNPL for groceries is best for short-term cash flow gaps when you can reliably cover all installments from your upcoming income. It helps spread costs without high-interest credit card debt, especially if using a no-interest, pay-in-4 plan for a larger grocery trip.