76% of U.S. citizens say that inflation has changed the way they buy shoes—and that’s especially frustrating when you consider that 68% of them buy those shoes to resolve foot pain.

Buy now, pay later shoes can make buying shoes less stressful.

Pay a bit to start, then pay the rest over time.

In this guide, I’ll let you know everything you need to know about BNPL shoes: where to get them, how to pay for them, and what to look out for before you finalize that purchase (and the clock starts ticking down to delivery day!).

Key Takeaways

- Helps Protect Cash Flow: Buy now, pay later shoe options let you get the shoes you need now without paying the full cost upfront.

- Pay In 4 Is The Most Common Setup: Most BNPL shoe plans use four payments over six weeks, often with no interest when payments are made on time.

- Longer Plans Can Cost More: Extended payment plans may give you more time, but they can also include interest, so the total cost matters.

- Common at Major Retailers: Many large shoe retailers offer BNPL at checkout, especially for online purchases.

- Works Best With A Plan: It’s smart to check the full repayment amount, make sure the payments fit your budget, and use reminders or autopay to stay on track.

What Buy Now, Pay Later Means When Shopping For Shoes

I have personally used BNPL for shoes and here’s why (embarrassing secret alert) – I have flat feet. This makes me prone to shin splints when I run or exercise, so high-quality running shoes are a must.

Unfortunately, they usually come with a higher price tag.

When you use buy now, pay later for shoes, you’re choosing to pay in installments instead of all at once. This works for sneakers, work shoes, boots, sandals—really, anything you’d like. Most online stores offer BNPL, and some in-person shops do, too.

The best part about using BNPL is having more control over the amount of money in my bank account. Purchases feel a lot less painful spread over 8 paychecks instead of just one. Sometimes, you can use BNPL even if you don’t have to, just to reduce the stress of a big hit to your account.

And particularly with a pair of shoes, which you use every day (and they can have a significant impact on your health), it can be smarter to pay more for something that fits well and lasts for years. BNPL makes that upfront cost more manageable.

How BNPL Shoe Payments Usually Work

Here’s what the process usually looks like, in my experience.

At checkout, instead of choosing a card, there’s usually a BNPL provider available. However, Sezzle is my favorite because I can use it whether it’s listed or not, thanks to the virtual card (accepted anywhere Visa is). There’s a quick approval, I agree to the plan, and payments are usually taken automatically on set dates.

It might sound like extra steps, but it really doesn’t take much longer than 30 seconds for the entire thing. That speed is one reason BNPL is popular. It’s a major perk to be able to decide if you can afford the shoes in full now or need to spread out payments—and, done correctly, both avenues are safe, effective options.

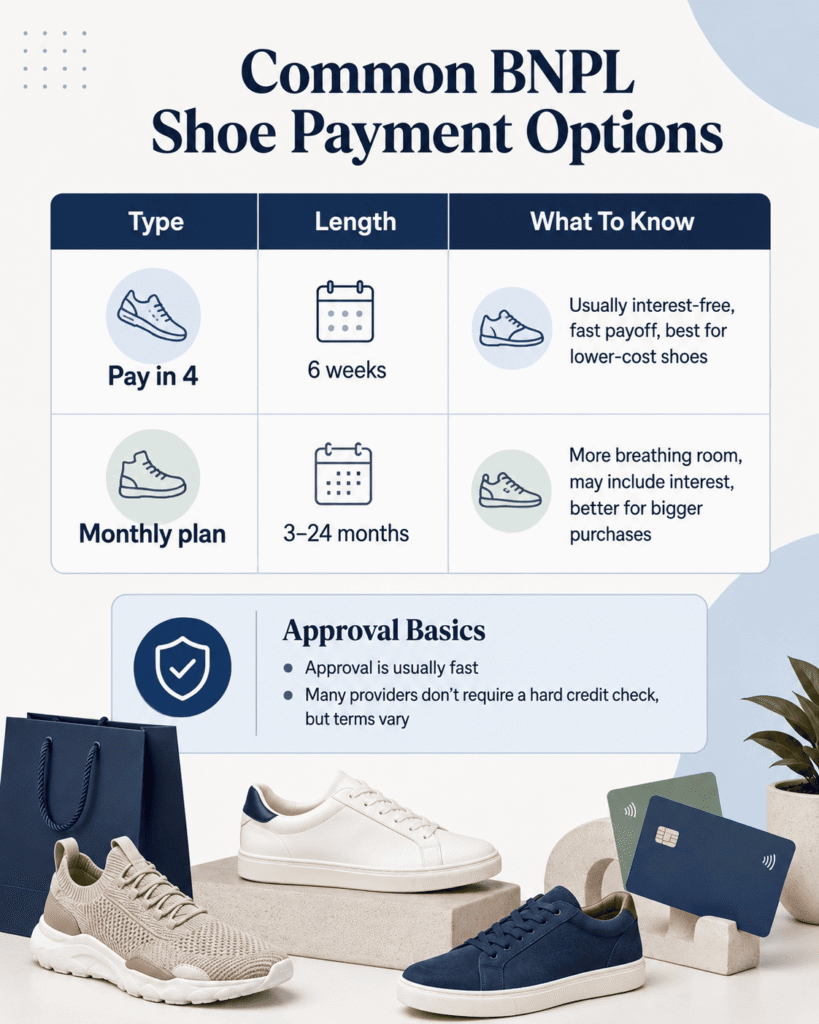

Common Payment Structures And Approval Basics

The most common plan is pay in 4: four equal payments over about six weeks. This is usually the best value since it often has no interest. The downside is that the payments are closer together and can feel bigger.

Some providers offer longer plans with 3, 6, 12, or 24 payments for some purchases. These can help with cash flow, but always check the total cost before confirming.

Here’s a quick comparison:

| Type | Length | Interest | Basics |

|---|---|---|---|

| Pay in 4 | 6 weeks | Often $0 | Lower-cost shoes, fast payoff |

| Monthly plan | 3–24 months | Sometimes charged | Bigger purchases, more breathing room |

Approval is usually fast, and many providers don’t require a hard credit check, but terms can vary.

Where You Can Buy Shoes With Buy Now, Pay Later

You can find buy-now, pay-later shoes at many well-known stores. Examples include Nike, DSW, Famous Footwear, Zappos, Hypebeast, and other retailers that work with BNPL providers, like Sezzle.

In most cases, BNPL is available at online checkout. As we’ve discussed, Sezzle has a virtual card feature that works in brick-and-mortar stores, alongside some other providers.

When I’m shopping for shoes on a budget, I check two things first:

- Whether the store offers pay in 4 or a longer installment plan

- Whether the final total changes because of interest or fees

This helps me stay focused and saves time.

Benefits, Risks, And Fees To Watch Before You Check Out

The main benefit of BNPL for shoes is flexibility. I can get the shoes now and keep more money in my account for things like groceries, gas, books, or rent. That’s important when money is tight, but the purchase is necessary.

Still, I always check the details. Some longer plans charge interest, and yes, late fees may apply. To be clear, though, this doesn’t make BNPL bad—it just means you need to pay attention during checkout and make sure you’re comfortable with the “real” price.

My rule is simple: if spreading out payments helps more than any extra cost hurts. It’s worth it.

How To Use Buy Now, Pay Later Responsibly For Shoes

I find BNPL works best when I use it with some structure. Shoes are easy to justify, especially for work, school, or comfort, so I try to be honest about what I’m buying and why (yes, easier said than done).

Before I check out, I always look at the total repayment amount, not just the first payment. I also make sure the due dates match my paycheck or other income. If a longer plan has interest, I decide whether the extra time is worth the cost—and sometimes, yes, it actually is.

A few habits help:

- Turn on autopay immediately

- Avoid stacking multiple BNPL shoe orders at the same time

- Leaving the item in the cart for 24 hours before committing

Ultimately, you know why you’re doing something, and whether it’s truly worth it or not. Trust yourself. You’ve got this.

Final Verdict

For me, buy now, pay later shoe options make sense because they reduce the upfront cost—and frankly, I think it makes it easier to get shoes that will last and not leave you with foot pain. It’s allowed me to prioritize what’s actually right for me and my life, not just to buy something cheap that falls apart in a month (which ends up being more expensive, anyway).

BNPL has been a game-changer, not just for my fashion but for my health, comfort, and quality of life.

FAQs

Buy now, pay later lets you purchase shoes and split the total cost into smaller payments over time instead of paying the full price upfront, often through online or in-store options.

At checkout, you select a BNPL provider, complete a quick approval, and then pay in scheduled installments automatically, typically with plans like four equal payments over six weeks.

You can find buy now pay later shoes at many retailers such as Nike, DSW, Famous Footwear, Zappos, and Hypebeast, using providers like Zip, Sezzle, or PayPal, mostly online but sometimes in-store.

BNPL offers flexible payments and can be interest-free if paid on time, helping with budgeting. However, risks include possible interest on longer plans, late fees, and convenience charges.

Responsible use includes reviewing the full payment plan, timing payments with your income, setting autopay or reminders, and avoiding multiple BNPL purchases simultaneously to prevent overextending your budget.

Yes, common options include paying in 4 installments over about six weeks, often interest-free, or longer monthly plans ranging from 3 to 24 months that may include interest, depending on the provider.