The average trip costs roughly $2,000 per person, per week.

Needless to say… Traveling isn’t cheap. Whether it’s a day trip or a month-long globetrotting trip, if you don’t plan ahead, you’ll feel the financial impact.

Travel now, pay later strategies can help: focusing on using BNPL services to spread payments over time, instead of spending a large lump sum at once (and breaking your budget as a result).

In this guide, I’ll lay out the top tactics and key strategies that actually work—as someone who’s used BNPL to travel myself (from Mexico to Greece)—so you can see the world without ever having to see the bottom of your piggy bank.

Key Takeaways

- Book Travel Now, Pay Over Time: Travel now, pay later lets you reserve flights, hotels, and vacation packages today while spreading the cost out over future payments.

- Plan Types Can Vary: Some travel financing options use short-term pay-in-4 installments, while others offer longer monthly plans that may include interest.

- Budget Fit Still Matters: The safest approach is choosing a plan that works with your actual monthly budget, not just the checkout payment.

- Compare Before You Commit: Looking at BNPL plans alongside credit cards and other payment options can help you find the best mix of cost and flexibility.

- Works Best With Careful Use: Travel now, pay later can make trips more manageable, but it works best when you understand the terms and avoid stacking too many plans at once.

What Travel Now, Pay Later Means for Flights and Trips

Travel now, pay later usually means using buy now, pay later financing to split your booking into set payments instead of paying all at once. You can use this for flights, hotels, vacation packages, and sometimes extras (think: car rentals, amenities, and meals).

There are usually two main types. One is pay in 4, which splits the cost into four payments over about six weeks, often with no interest. The other is a longer monthly plan that may charge interest.

Which should you choose? Honestly, both options can work. Pay in 4 is good if you can manage larger payments quickly. Longer plans are better if you need smaller payments and more time.

| Option | How it usually works | Best for | Watch out for |

|---|---|---|---|

| Pay in 4 | Four payments over a short period, often interest-free | Travelers who can handle larger payments quickly | Payments come fast |

| Monthly plan | Smaller payments over a longer term, may include interest | Travelers who need more breathing room | Higher total cost |

How Travel Financing Works From Checkout To Monthly Payments

From my experience, at least, the process is usually quick and easy.

At checkout, you might see a BNPL option like Flex Pay, Zip, or another pay-monthly offer. Then, you fill out a short application. Some companies just do a soft credit check, but others might look at your credit more closely for longer plans.

If you’re approved, the BNPL company pays the airline, hotel, or travel site for you. Meanwhile, you pay the provider back on the schedule you set, often using autopay. With pay-in-4, the first payment might be due right away. With monthly plans, you might have more time, but always check the interest amount before you confirm.

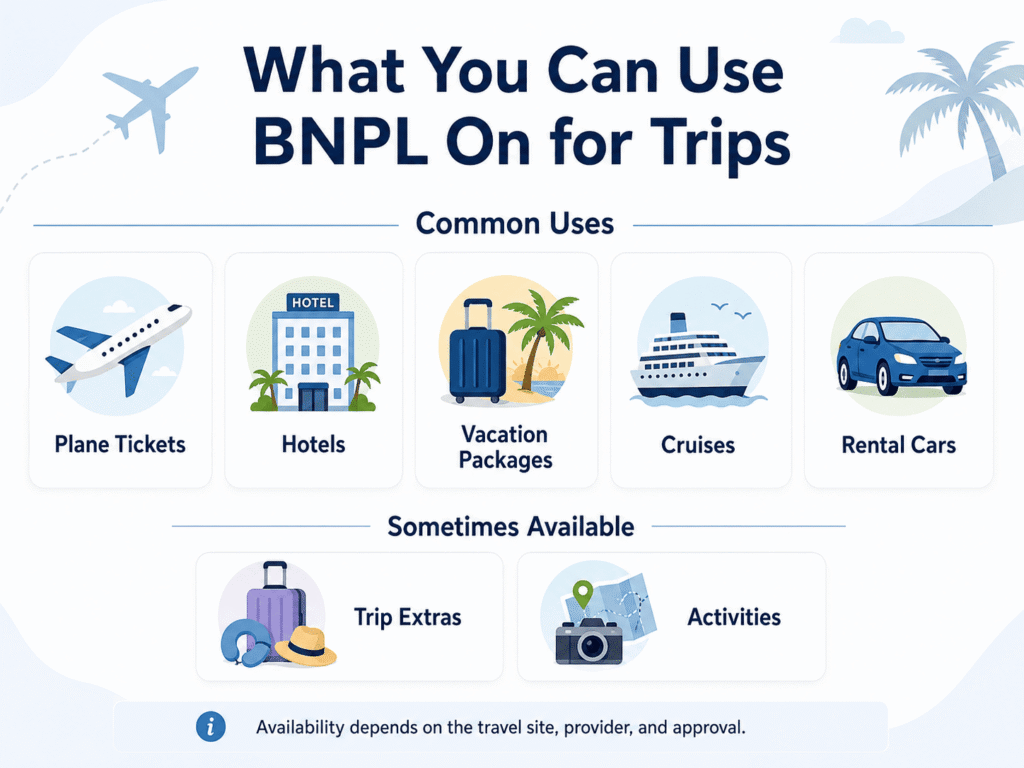

Where You Can Use It For Airfare, Hotels, And Vacation Packages

Travel financing is available in more places than many people realize. Some airlines and online travel agencies offer BNPL at checkout. Providers like Sezzle appear with certain airline bookings, but you can also take advantage of their virtual card service with any company that accepts Visa payments.

You can also use it for hotels and vacation packages. Some companies let you finance the whole trip, not just the flight—you can use it for cruises, hotels, or rental cars. However, the specifics depend on the merchant, the provider, and your approval.

The Main Benefits And Risks To Weigh Before You Book

The main benefit is flexibility. You don’t have to pay everything at once, so you can spread out the cost and match payments to your paydays. This makes it easier to manage trips you need to take and makes big vacations feel less overwhelming.

Another benefit is locking in today’s price before it increases. Fixed payments also make planning easier. Personally, I feel a lot more relaxed knowing the price won’t randomly change on me when I’m not looking.

The main downside is cost. Some monthly plans charge interest, and the rates can be high. You might also still be paying after your trip is over. That’s not always a problem (in fact, I think it’s expected), but it’s important to know what you’re agreeing to.

How To Use Travel Now, Pay Later Responsibly

Using these plans responsibly is simple. Make sure the payments fit your real monthly budget, not just what you hope you can afford. Then check the total cost, including any interest or fees, and decide if it’s worth it.

Pay in 4 is often the best option if you can handle the quicker payments, since it’s usually interest-free. But paying some interest isn’t always bad if it gives you more room in your monthly budget. Just make sure you know the exact amount before you book.

Using autopay helps, and it’s also smart to avoid having multiple plans at the same time.

Let’s sum it all up.

Before you book, make sure to:

- Check that the payments fit your real monthly budget

- Review the total cost, including interest and fees

- Compare pay-in-4 with monthly financing

- Use autopay if it helps you stay on schedule

- Avoid stacking multiple travel payment plans at once

Final Verdict

Travel now, pay later can be a smart way to manage travel costs. It helps protect your cash flow, lets you book trips sooner, and makes travel possible. If you check the real cost and pick terms that fit your budget, it’s a helpful option.

Personally, even if you don’t really need to use BNPL, it definitely feels less stressful knowing you don’t have to pay as much all at once—and you can spend that energy enjoying your trip instead.

FAQs

What does travel now, pay later mean for booking flights and vacations?

Travel now pay later means using buy now, pay later (BNPL) financing to split the cost of flights, hotels, or vacation packages into fixed installments instead of paying the full amount upfront.

How does travel financing typically work at checkout?

At checkout, you select a BNPL option like Flex Pay or Zip, complete a brief application, and if approved, the provider pays the travel merchant. You then repay the BNPL provider in scheduled installments, often via autopay.

Where can I use travel now pay later options?

Travel financing is available for airfare through many airlines and online agencies, for hotels and full vacation packages, and sometimes for car rentals or cruises using BNPL virtual cards accepted where Visa is accepted.

What are the main benefits and risks of using travel now pay later?

Benefits include spreading out travel costs, locking in prices, and fixed payments. Risks involve potential interest charges up to 36% APR, ongoing payments after travel, and fees or credit impact if payments are missed.

How does travel now pay later compare to credit cards for financing trips?

Short-term BNPL plans often have 0% interest with faster payments, while credit cards offer rewards and protections, but can carry high interest if balances aren’t paid quickly. The best choice depends on cost, timing, and budget flexibility.

How can I use travel now pay later options responsibly?

Calculate total costs including interest, ensure payments fit your budget, prefer low- or no-interest plans, use autopay to avoid missed payments, avoid overlapping BNPL plans, and consider layaway-style plans if you want to avoid credit.